“There’s no such thing as a free lunch.” – Milton Friedman (1975)

It is often stated that a key benefit of paying for a managed account is the personalized savings advice it provides.

This benefit, though frequently discussed and sometimes quantified, is rarely measured over time. So how “free” is this benefit? To us, it calls to mind Milton Friedman’s famous adage. The phrase “free lunch” refers to the once-common tradition of saloons in the United States providing a free lunch to patrons who had purchased at least one drink. Many foods were high in salt (e.g., ham, cheese and salted crackers), so those who ate them ended up buying a lot of beer.

Rudyard Kipling, in 1891, acknowledged that neither a person nor a society can get “something for nothing.” So, when it comes to the personalized savings advice that comes with managed accounts, what value do they really provide, and are there hidden costs?

EXECUTIVE SUMMARY

MANAGED ACCOUNTS SAVINGS ADVICE: COSTS AND ALTERNATIVES

In this study, we attempted to ascertain the on-going value of savings advice by comparing the gains a participant realizes from paying annually for managed account services to automatic escalation. Automatic escalation is a common design feature of a defined contribution (DC) plan that incurs no additional cost to the participant.

KEY FINDINGS

Managed accounts that offer savings advice add value for participants – but that value declines over time.

We believe that an advisor should receive full credit for the initial savings advice provided to a participant through managed accounts, followed by proportional credit for any subsequent increases in savings stemming from the participant’s salary raises. This approach fairly assesses the one-time savings advice value by recognizing every proactive change in a participant’s savings behavior.

However, the bulk of the savings advice benefit for a participant materializes in the first year (and is further augmented by the annual compounded market returns on those savings). Starting in the second year, the primary driver for subsequent savings growth is limited to any merit increases in pay.

However, the cost of savings advice does not decline.

After including the fee charged by the managed account provider, savings advice has a negative return on investment after the first year. This is mainly because managed accounts fees are charged based on a participant’s total assets rather than on changes in their annual savings.

At a minimum, the structure of managed account fees and savings advice should change.

We believe savings advice should be a one-time charge commensurate with the incremental change in a participant’s savings rate, rather than a recurring expense. Therefore, it’s essential that managed account fees are either reduced to reflect the actual value received by participants or structured in a way that those continuing to pay for managed accounts beyond the first year see a corresponding increase in value through other areas, such as investment and/or spending advice.

Ultimately, there is a better, cheaper alternative.

A more effective solution for plan sponsors looking to broadly improve savings lies in enrolling participants in auto-escalation. Should a plan sponsor opt to implement auto-escalation by 1% annually up to a 10% ceiling, we estimate a compound growth in participants’ DC assets of more than 14% after 15 years. In addition, it’s a conservative estimate to expect that over 50% of participants would remain defaulted in the auto-escalation program, representing a significant improvement compared to the relatively small group served by managed accounts.

Let’s take a closer look at these conclusions.

WHAT IS SAVINGS ADVICE?

When we refer to someone offering or receiving savings advice, what exactly are the expectations?

The general assumption is that a managed account provider will assess a participant’s projected retirement income and, if it seems likely to fall short of their retirement income objective, advise a higher savings rate to meet the participant’s goals.

Optimally, that same day, the participant both accepts and implements the savings advice given by the managed accounts provider. It is crucial to note that the responsibility to change their savings rate ultimately rests with the participant. The managed account provider does not have the discretion to make this change on the participant’s behalf.

OUR ANALYSIS

In this study, we are assessing the impact of three scenarios on savings advice:

- two commonly cited recommendations of 1% and 2%1, and

- a more significant 5% savings increase.

This paper primarily focuses on the most cited 2% savings advice, with details of the full analysis available in the appendix.

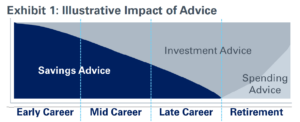

Savings advice is generally seen as most beneficial for individuals in the early to mid-stages of their career, due to their longer time horizon to save (Exhibit 1). Concentrating on this demographic is logical because their investment period allows for substantial growth. Also, managed account investment advice is less impactful for this demographic as participant portfolios tend to look like target date funds with high equity allocations. Our analysis assumes at least a 15-year time horizon.

In this analysis, we assume a participant receives the full benefit of the managed accounts savings advice on the first day they agree to start paying for the service. This allows us to gauge the maximum utility that can be derived from the savings advice. That said, we recognize that although a person may pay for managed accounts on day one, there may be some lag due to the speed of engaging with the system, entering personal information, accepting, and implementing the savings advice. Therefore, the actual return on a participant’s investment for savings advice will be lower than our analysis indicates, considering the time value of money and the advance payment for advice before any financial benefit from savings materializes.

1 The Impact of Managed Accounts on Participant Savings and Investment Decisions (2019: David Blanchett)

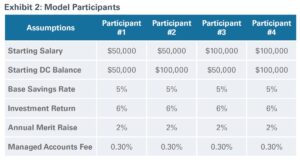

OUR MODEL “PARTICIPANTS”

We constructed models for four distinct participant scenarios (Exhibit 2). These scenarios were selected to evaluate if a participant’s starting salary, starting balance, or a combination of the two had a material impact on the value of savings advice from a managed account. Specifically, our assessment investigated whether the starting balance in a DC plan that is equal to a participant’s salary, half of their salary, or double their salary made a difference in valuing the benefit of savings advice.

THE MARGINAL BENEFIT OF SAVINGS ADVICE BEFORE FEES

For participants #1 and #2, earning an annual salary of $50,000, a 2% increase in savings led to an additional $1,000 saved in the first year; participants #3 and #4, with an annual income of $100,000, saw an additional $2,000 due to the same 2% savings increase. Assuming these participants stay the course, they will continue saving an extra $1,000 or $2,000 annually until retirement without needing more advice or taking further action.

Is that the whole picture, though? Hopefully not.

It is expected that these participants will apply the 2% savings increase to any future salary hikes. As an example, after year one, participant #1 could see incremental new savings, ranging from $20 to $55 annually, growing from the second year to the 15th year. Moreover, beginning in the second year, participant #1 could accrue an additional $60 up to $160 in the 15th year, thanks to compounding market returns on all their additional savings until retirement.

So, how do you measure the benefit?

We recognize there are two key schools of thought on evaluating the impact of savings advice.

- The first says that advisors should be given continuous credit for savings advice, year after year.

- The second contends that advisors should receive full credit for the advice in year one, followed by proportional credit for any subsequent increases in savings stemming from participants’ salary raises.

We advocate for the latter approach as it more equitably assesses the value of one-time savings advice by acknowledging each proactive change in a participant’s savings behavior. The first approach, which attributes value to the mere inertia of an initial change in savings rate against the original salary, does not align with the dynamic nature of actively managed accounts.

Exhibit 3 shows the impact of savings advice under the second, preferred approach. The bulk of the savings advice benefit (i.e., the additional $1,000 or $2,000) materializes in the first year. From the second year onward, the potential for merit increases becomes the driving force behind future increases in savings, which is further augmented by the annual compounded market returns on those savings.

Participant #1 receives $1,000 in savings benefit in the first year; $80 in benefit in the second year 1; $85 in the third year; $90 in the fourth year, and so on (Exhibit 3).

THE RETURN ON INVESTMENT (ROI) OF SAVINGS ADVICE AFTER FEES

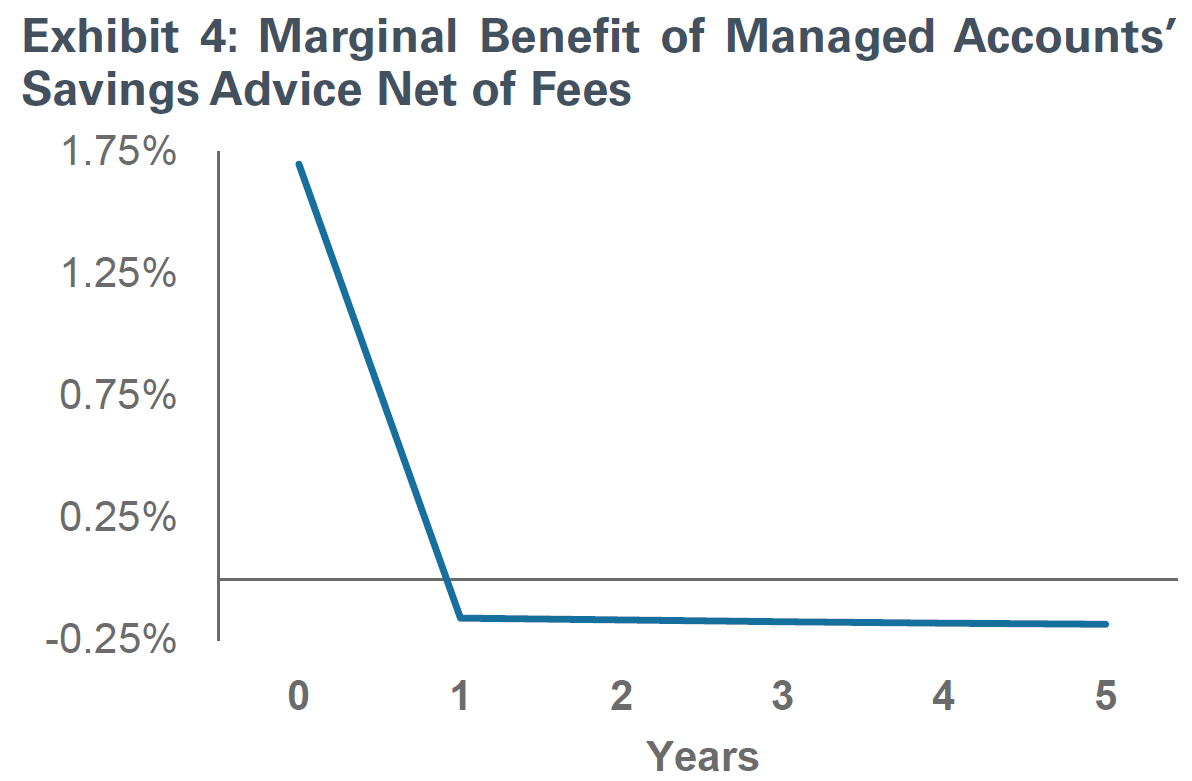

After the benefit was calculated, we computed the cost of savings advice. Surprisingly, when the fee charged by the managed account provider was included, savings advice had a negative return on investment after year one. Exhibit 4 shows the marginal benefit of savings advice net of fees.

The reason for the negative ROI is that the managed account fee was based on the participant’s DC assets. As the participant’s assets grew faster than their salary, the incremental year-over-year rise in fees was greater than the incremental year-over-year increase in the participant’s salary, and therefore savings. This was especially true for participants younger than age 40 whose managed account investment allocation would have high exposure to equities, similar to a target date fund.

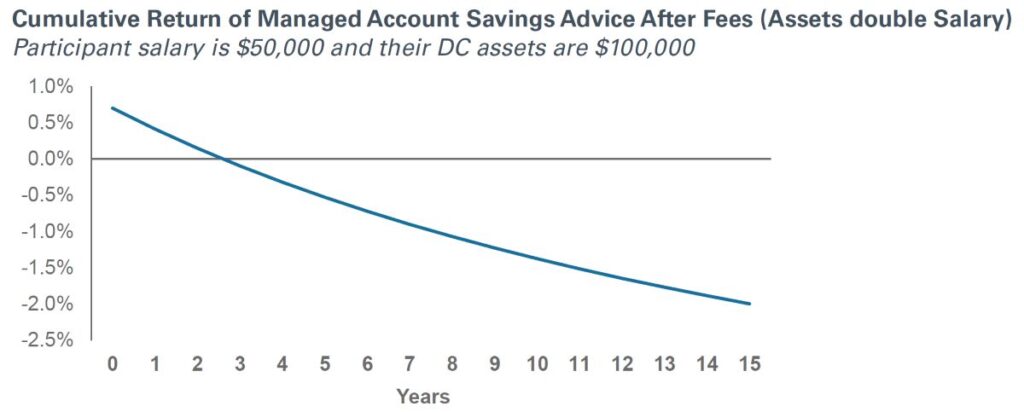

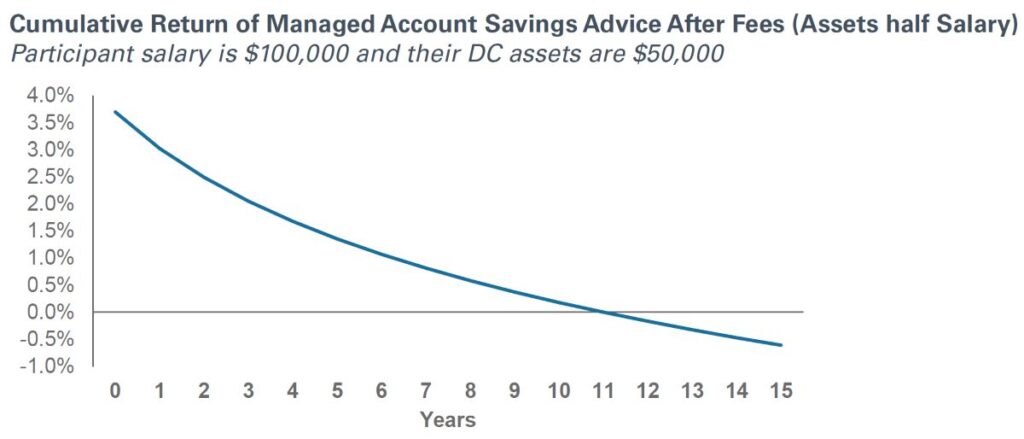

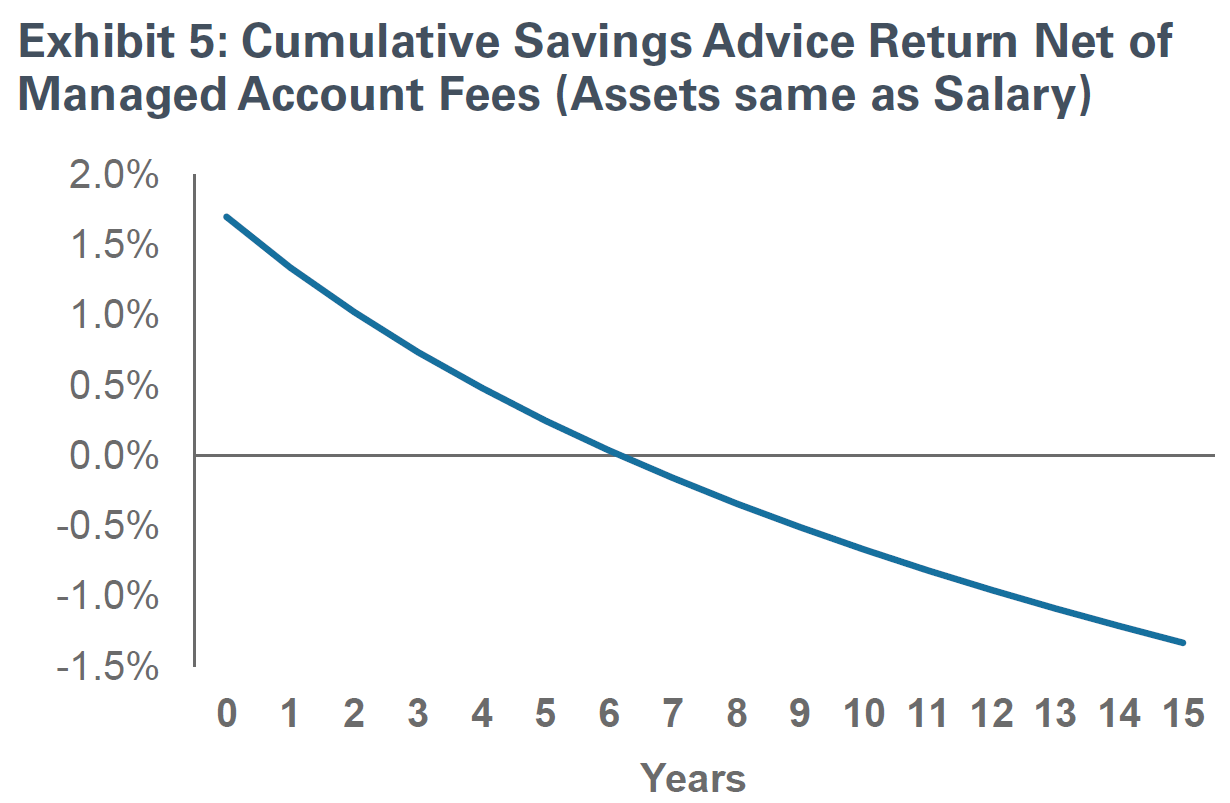

Diving into the details, let’s assume the fee a managed accounts provider charges for all services (e.g., savings advice, investment advice, spending advice) is 0.30% per year against a participant’s DC assets. If the participant’s salary and DC assets are the same at the start (i.e., $50,000 salary and $50,000 DC assets or $100,000 salary and $100,000 DC assets), then the marginal benefits from only savings advice will remain positive until about year six when the managed account’s fees of 0.30% salts away the entire benefit of the initial savings advice (Exhibit 5). This underscores the trend of diminishing returns from savings advice when managed account fees are factored in.

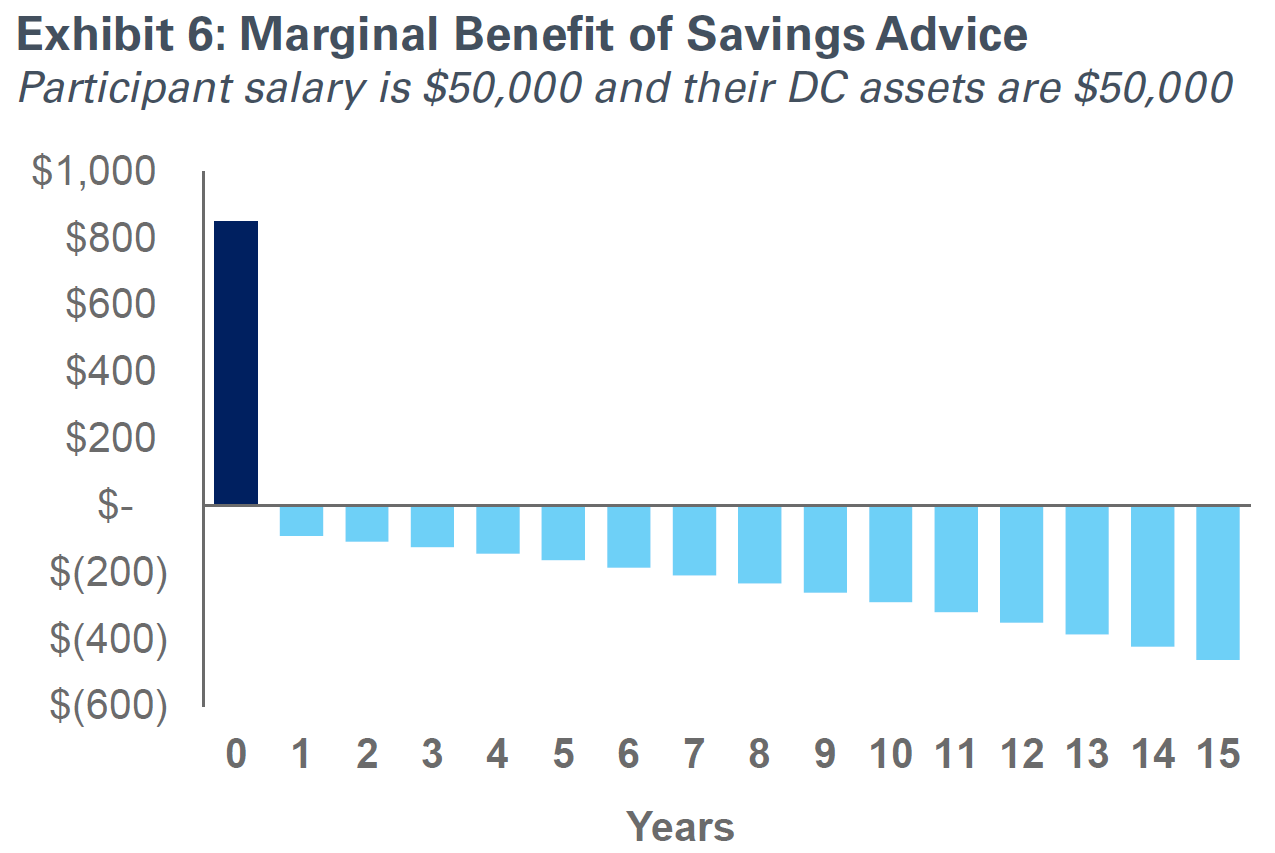

Exhibit 6 shows that the cost of a managed account for participant #1, though initially modest, scaled with asset growth – starting from an approximate cost of $150 and escalating to $1,000 per year by year 15. In contrast, the value derived from savings advice started at $80 after year one and increased to approximately $190 by year 15. Ultimately, the net marginal benefit of savings advice after the cost of managed accounts was a negative $90.

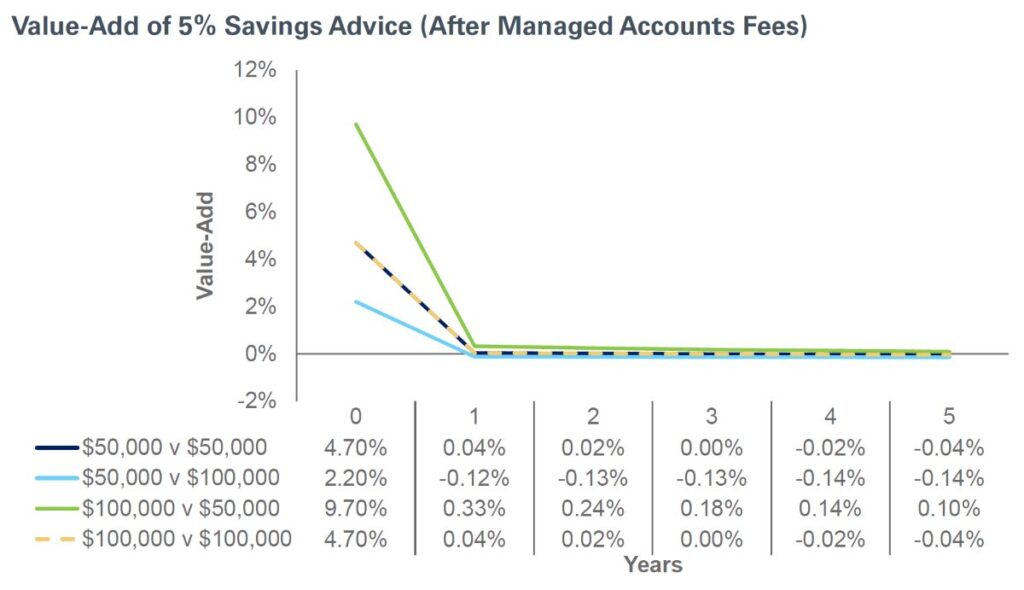

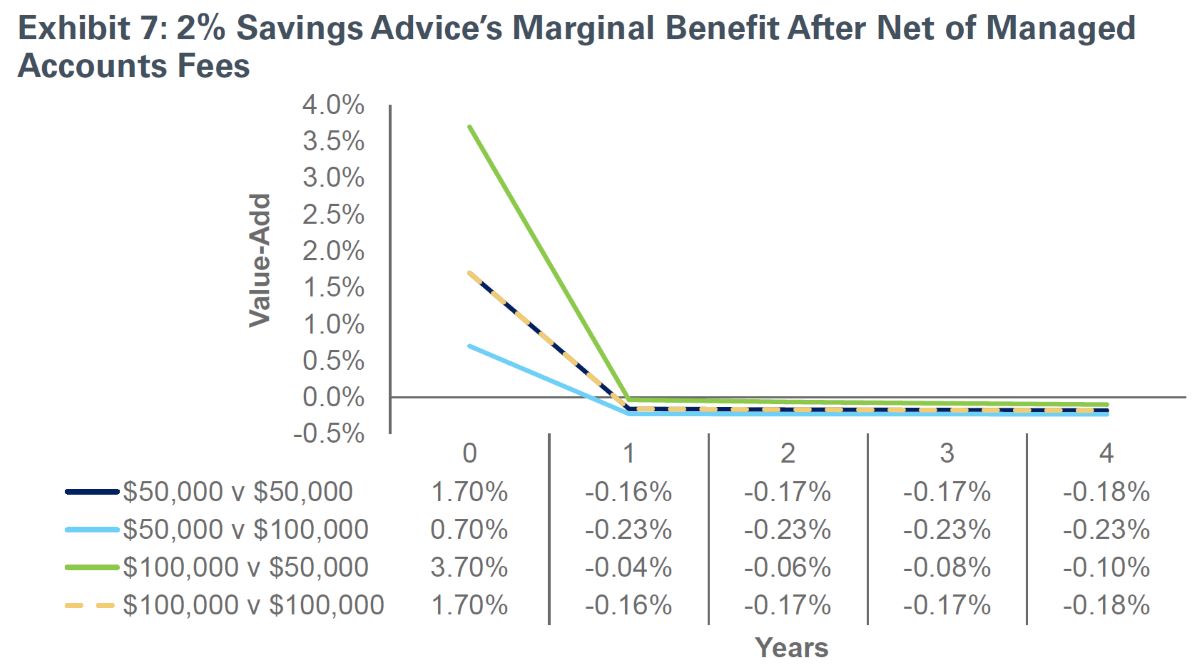

To determine if this trend persists irrespective of the participant’s income or savings, we analyzed all four participant scenarios. As a reminder, the scenarios set each participant’s DC assets at various levels relative to their starting salary (equal to, half of, and twice the value) and factored in a 2% annual merit increase, a 2% improvement in savings from advice, a managed accounts fee of 0.30%, and a 6% average rate of return on investments.

The analysis across the four participant scenarios showed a benefit from savings advice before accounting for the costs. This benefit, however, was quickly eroded after year one in all scenarios, once managed account fees were incorporated (Exhibit 7). Participants with assets greater than their annual salary face the most significant cost impact once fees are applied.

A key factor influencing these findings is that managed account fees are charged based on a participant’s total assets rather than on changes in their annual savings. This misalignment of interest is a key reason we support the second school of thought when evaluating the value of savings advice. Advice fees should be aligned with the advice provided, suggesting that savings advice should be a one-time charge—rather than a recurring expense—commensurate with the incremental change in a participant’s savings rate.

Therefore, it is essential that fees are either reduced to reflect the actual value received by participants or structured in a way that those continuing to pay for managed accounts beyond the first year see a corresponding increase in value through other areas, such as investment and/or spending advice. We will be exploring the benefits of personalized investment advice in a separate paper.

AUTO-ESCALATION: A BETTER, CHEAPER OPTION

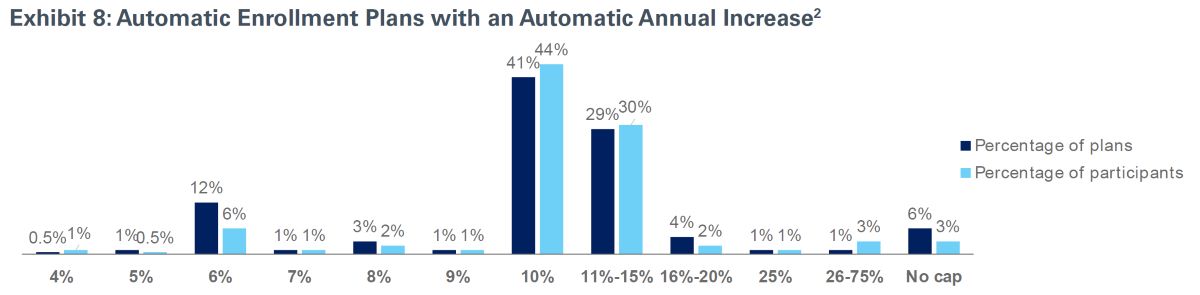

When it comes to improving the outcomes for participant savings, there is a better option staring plan administrators in the face: implementing auto-escalation as a plan design feature. Recent findings reveal that close to 69%2 of DC plans offer auto-escalation, with most plans auto escalating participant savings rates up to between 10% to 15%2. This approach not only simplifies the savings process, but also yields a far higher savings rate compared to the average outcomes from managed accounts savings advice.

Currently, less than 10% of participants opt into using managed accounts3, indicating that managed accounts’ ability to meaningfully impact participants may be constrained to a small universe.

A more effective solution for broadly improving savings lies in enrolling active participants in auto-escalation, increasing their annual savings rate by 1% or 2% per year until they hit a targeted savings rate between 10% and 15%. It is a conservative estimate that over 50% of participants would remain defaulted in the auto-escalation program, representing a significant improvement compared to the relatively small group served by managed accounts.

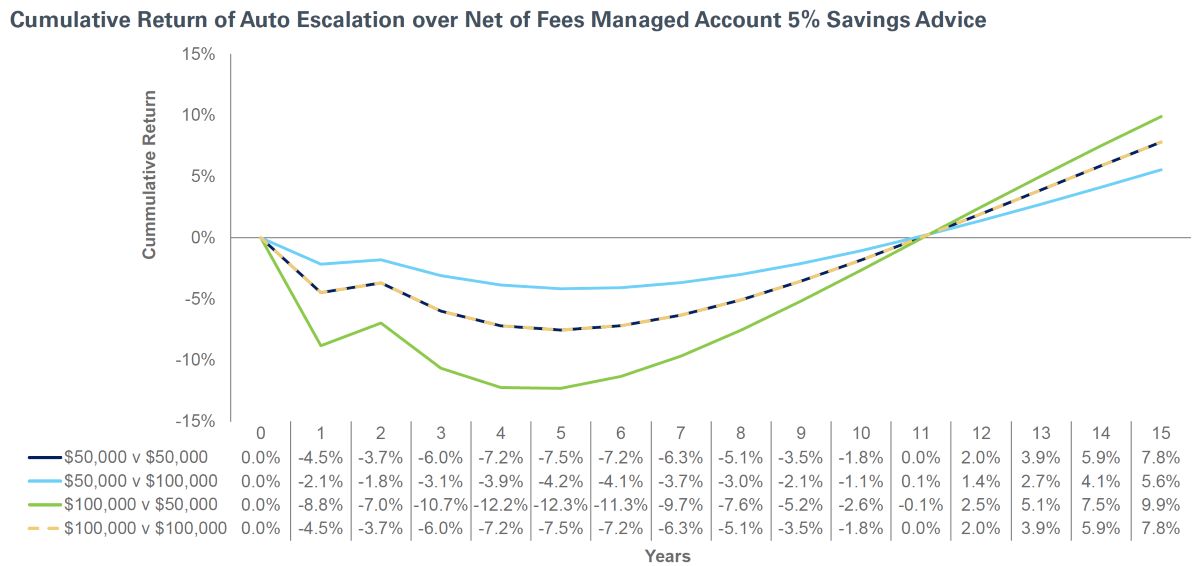

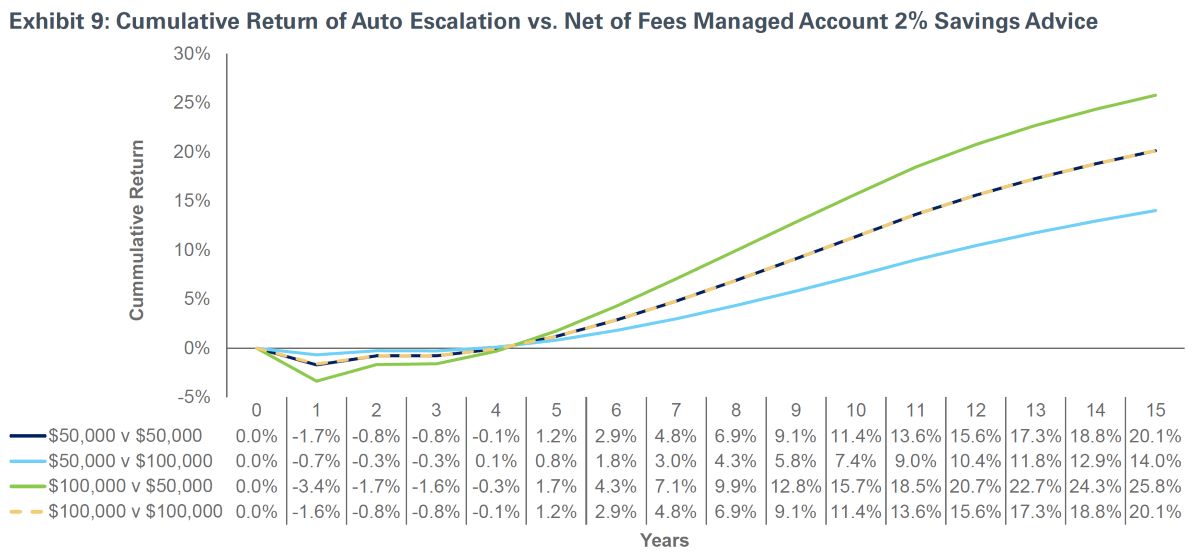

We expanded our study to evaluate a situation where a participant moves from incurring fees for savings advice to enrolling in auto-escalation. The results indicated that by the fourth year, this participant gains more value from auto-escalation than from the savings advice provided through managed accounts (Exhibit 9).

Remarkably, in this scenario, what started as a diminishing benefit from savings advice—due to managed accounts fees—transforms into an accelerating year-over-year benefit from auto-escalation. Should a plan sponsor opt to implement auto-escalation by 1% annually up to a 10% ceiling, we estimate a compound growth in participants’ DC assets by over 14% after 15 years.

2 How America Saves (Vanguard 2023)

3 NEPC’s 18th Annual DC Plan Trends & Fees Survey

CONCLUSION

Unfortunately, the data suggest that savings advice is no free lunch. We find the data in support of auto-escalation compelling, and we believe auto-escalation should be the primary solution for increasing participant savings due to its proven results and cost efficiency.

Furthermore, within the industry, we’re now able to reassess the value proposition of savings advice through managed accounts, considering that there is a no-cost alternative that achieves broader adoption and offers substantial benefits. To learn more or to discuss this in greater detail, please contact your NEPC consultant.

APPENDIX