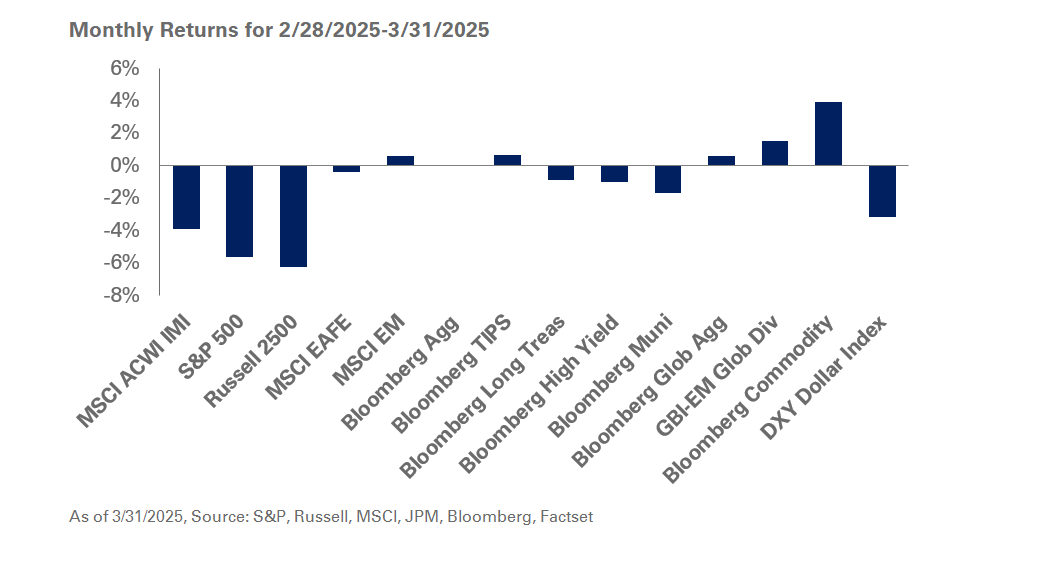

Last week saw the S&P 500 Top 10 Index drop more than 10%—technically qualifying as a market correction—after hitting a peak on February 19th. As investors wonder if the recent losses are a warning of more ominous times to come, we turn to Phillip Nelson, NEPC’s Head of Asset Allocation, for answers.

- Should investors be worried about the market correction?

While investor sentiment has declined considerably since the start of the year and markets appear more volatile, it is important to remember that corrections are a fairly common occurrence in a calendar year. Following two consecutive years of gains of 20% or more for the S&P 500 Index, a minor correction is a healthy adjustment in valuations for markets. The fall in investor sentiment has had a greater impact on the Magnificent 7 and names with above average price-to-earnings multiples relative to a diversified basket of U.S. equities.

Despite the decline in bullish investor sentiment and falling consumer sentiment, earnings expectations for the S&P 500 remain healthy with year-over-year earnings growth for 2025 sitting above 10%.

- What is NEPC’s investment advice to investors?

With a more severe price decline from the S&P 500 and forward P/E multiples falling, additional equity rebalancing opportunities may arise. We encourage investors to maintain sufficient liquidity levels in portfolios. In addition, we highly recommend maintaining safe-haven fixed-income exposure at strategic targets to protect against economic downturns and market shocks.

We encourage embracing portfolio diversification and holding to long-term strategic allocation targets. Over time, we believe investors will be well-served by remaining disciplined and pursuing investment opportunities as a liquidity provider.

- Are concerns around tariffs justified?

We do acknowledge the uncertainty swirling around the impact of the Trump administration’s tariff policies on the U.S. economy. While equities are highly reactive to the prospect of tariffs, it is too early to assess the economic impact of tariffs and how they are applied to imported goods, and/or which imports may be exempt.

In our view, tariffs represent a consumption tax and do not necessarily have a direct inflationary impact as consumers adjust spending habits in response. We still believe that U.S. tariff policies will have a subdued economic impact but an escalation that restricts the flow of goods would pose a broader economic risk.

- Should the markets be worried about a recession?

Consumer spending and balance sheets remain healthy in the United States, and it is not an oversimplification to say that the U.S. consumer is the growth engine for the world. Economic and investor sentiment can slow economic activity but, generally speaking, spikes in uncertainty without shifts in the underlying data tend to be temporary.

Our key focus in the coming months is to gauge to what extent cuts in the federal workforce may be a catalyst for job attrition in the private sector. For the U.S. to sink into a recession, the scale of job losses in the private sector will have to be in the millions; this seems unlikely given the relatively healthy sales and earnings guidance we see from many public companies at this time. While the likelihood of a recession has edged up since the start of the year, we do not believe there is a high risk at present.

Related Insights