Global Equities

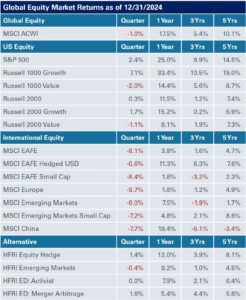

Stocks were a mixed bag in the fourth quarter with domestic equities outperforming their international peers. U.S. equities led performance with the S&P 500 Index posting gains of 2.4%; during the same period, the Russell 2000 returned a modest 0.3%.

International and emerging markets lagged with the MSCI EM Index losing 8% for the three months ended December 31; the MSCI EAFE Index was down 8.1% following two rate cuts by the European Central Bank which added to market volatility and bolstered the U.S. dollar.

Meanwhile, U.S. private equity fundraising activity totaled $287.3 billion in 2024, according to PitchBook, falling short of the $394.8 billion raised the year before. U.S. venture capital fundraising also experienced a slowdown as totals fell to $76.1 billion this year from $97.5 billion in 2023. In terms of number of funds, 316 private equity and 508 venture funds closed fundraises through 2024 compared to 685 private equity funds and 937 venture funds the year before.

New deal activity in U.S. private equity totaled $838.5 billion this year, up from $703 billion in 2023. U.S. venture capital new deal activity rebounded significantly in the fourth quarter, resulting in year-end deal value totaling $209 billion across 15,260 deals, surpassing pre-pandemic and 2023 totals. Exits in private equity-backed companies grew steadily during the quarter, with total year-end exit volume reaching $416.7 billion across 1,502 deals, representing a three-year high driven, in part, by lower interest rates. Exit activity was up slightly in 2024, reaching $149.2 billion across 1,259 deals compared to $120 billion across 1,143 deals in 2023; however, 2024 levels still fell short of pre-pandemic activity.

Global Fixed Income

The last quarter of 2024 saw a reversal in Treasuries, as the market see-sawed in a relatively wide trading range. Yields backed up significantly at year-end after the summer rally in Treasuries. Despite the two additional cuts by the Federal Reserve, which left the Fed Funds rate at a target range of 4.25%- 4.50%, five- and 10-year notes sold off. Credit spreads were generally tighter, remaining well below long-term median levels.

The last quarter of 2024 saw a reversal in Treasuries, as the market see-sawed in a relatively wide trading range. Yields backed up significantly at year-end after the summer rally in Treasuries. Despite the two additional cuts by the Federal Reserve, which left the Fed Funds rate at a target range of 4.25%- 4.50%, five- and 10-year notes sold off. Credit spreads were generally tighter, remaining well below long-term median levels.

For the three months ended December 31, the spread on investment-grade corporate bonds tightened nine basis points, while high-yield corporate bonds narrowed eight basis points. During this period, emerging markets debt (hard currency) led the charge, tightening 77 basis points.

The yield on the 10-year Treasury rose 80 basis points to end the quarter at 4.58%, while the 30-year Treasury bond yield increased 66 basis points to yield 4.78%.

Despite the selloff in the fourth quarter, most major fixed-income indexes posted modest gains for the year. The Bloomberg Aggregate Bond Index fell by 3.06% in the fourth quarter, resulting in an annual return of 1.25%; high-yield debt fared better, with the Bloomberg U.S. Corporate High Yield Index gaining 0.17% in the fourth quarter, bringing annual returns to 8.19%.

Real Assets

Liquid real assets posted mixed returns in the final quarter of 2024. The Bloomberg Commodity Index lost a modest 0.4%; meanwhile, crude oil bounced back with a 4.3% return after a weak third quarter, ultimately finishing the year flat. Midstream led all real asset returns in the three months ended December 31, with the Alerian Midstream Index up 13.5%. Gold (spot price) was flat in the fourth quarter at -0.4%, but posted a solid 27.2% return for the year.

Liquid real assets posted mixed returns in the final quarter of 2024. The Bloomberg Commodity Index lost a modest 0.4%; meanwhile, crude oil bounced back with a 4.3% return after a weak third quarter, ultimately finishing the year flat. Midstream led all real asset returns in the three months ended December 31, with the Alerian Midstream Index up 13.5%. Gold (spot price) was flat in the fourth quarter at -0.4%, but posted a solid 27.2% return for the year.

Global natural resources struggled, down 12.4% in the fourth quarter, ending the year in the red with losses of 9%. The S&P Global Infrastructure Index fared better, losing 2.3% in the fourth quarter and posting gains of 15.3% for 2024. NEPC maintains a favorable view of natural resources and infrastructure and we continue to prefer private markets when it comes to implementing infrastructure in an investment portfolio.

Real estate investment trusts had a challenging fourth quarter, with the NAREIT Global REIT Composite Index down 8.9%, bringing full year returns to a modest 2.8%. The NCREIF ODCE posted a preliminary gross return of 1.16%, inclusive of 0.14% of asset appreciation, marking the first quarter in two years of positive asset appreciation for the NCREIF ODCE.

Real estate debt—despite its more conservative position in the capital stack—remains a bright spot as higher interest rates, impending loan maturities, and pullback from traditional lenders have led to higher return expectations that rival potential gains from value-add real estate equity strategies. On the other end of the spectrum, opportunistic and distressed real estate investors may be able to capitalize on these same market dynamics to acquire high-quality assets suffering from capital structure issues.

Managers of secondaries have also benefitted from this trend especially as general partners seek creative solutions to recapitalize assets that have a limited buyer pool. NEPC remains committed to a barbell approach to investing in closed-end real estate funds.

Private infrastructure strategies continue to garner increased interest among investors, and we are particularly constructive on tailwinds driving digital and communications infrastructure, renewable energy and energy transition strategies. We also view infrastructure secondaries as broadly attractive and are supportive of infrastructure debt for investors with a lower risk tolerance or a preference for income.