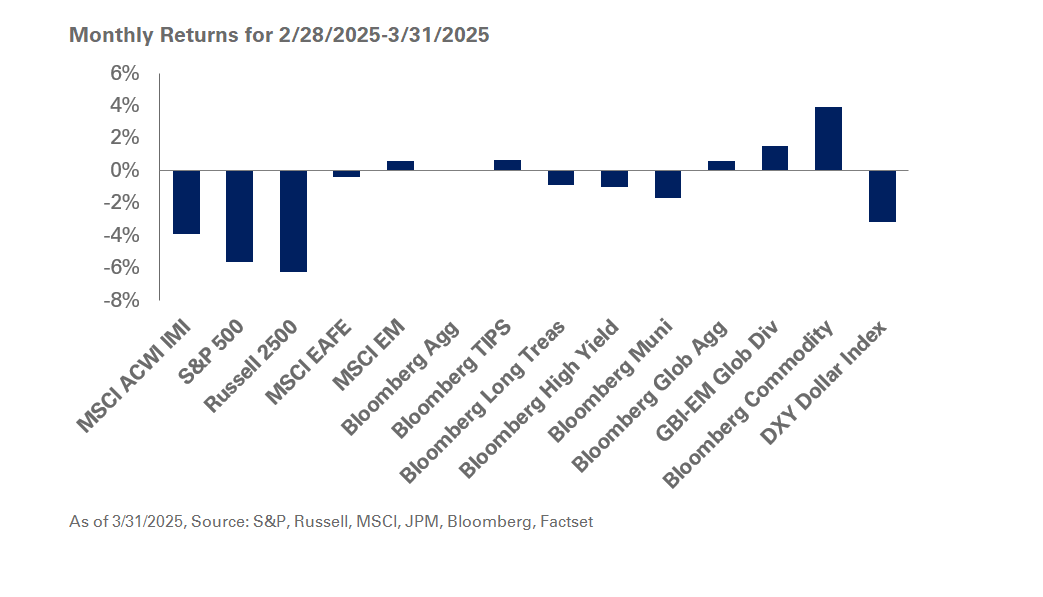

Equities retreated in March amid a flurry of headlines around tariffs, and weakening sentiment among households, consumers and small businesses. The heightening concern around growth and inflation is in contrast to an otherwise solid showing by the U.S. economy: headline consumer price inflation for February rose a modest 0.2% reflecting a 2.8% increase over the past year. Meanwhile, employment data for March exceeded forecasts with the economy adding 228,000 jobs, while weekly jobless claims remain stable. Despite the robust economic data, forward-looking expectations are starting to price increased uncertainty around tariffs, their rates, implementation, scope and and their potential impact on the U.S. economy.

Equities bore the brunt of the risk-off sentiment with U.S. stocks taking the biggest hit. Large-cap stocks finished March with losses of 5.6%; value stocks, down 2.8%, outperformed growth equities which lost 8.4%. Small-cap stocks continued to lag, down 6.3% for the month. Outside the U.S., dollar weakness provided a tailwind to returns, with the MSCI EAFE Index down a moderate 0.4% and the MSCI Emerging Markets Index leading performance with gains of 0.6%.

The Federal Open Market Committee met in March and kept interest rates unchanged though it did announce a slower pace to its quantitative tightening program under which it allows its Treasury holdings to mature and roll-off its balance sheet—reducing the monthly cap from $25 billion to $5 billion. Fed Chair Jerome Powell indicated the Committee is in a wait-and-see mode as uncertainties around tariffs play out. The updated Fed dot plot survey of interest rate expectations of Committee members showed no changes from the last survey published in December 2024, with the median interest rate projection indicating two interest cuts in 2025.

Fixed-income returns were mixed in March given modest steepening in the Treasury yield curve. The 10-year Treasury yield remained relatively flat at 4.2%. Credit markets saw spread levels widening in-step with the equity sell-off as investment-grade spreads rose seven basis points to 94 and high-yields spreads jumped 67 basis points to 347 basis points.

Commodities provided diversification in March with the Bloomberg Commodity Index up 3.9%. Commodity prices were broadly higher for the month, excluding grains; the primary driver of the strong performance was spot gold, which saw prices rising to over $3,100/oz.

Given recent market dynamics, we encourage investors to remain disciplined and stick to long-term strategic asset allocation targets. We believe volatility is likely to persist until greater clarity emerges around the administration’s policy on tariffs and tariff rates. As such, we recommend investors hold adequate liquidity on hand for cash flow needs and take advantage of opportunities to rebalance back into the S&P 500. Finally, we suggest maintaining neutral duration positioning relative to strategic targets as bond yields are pricing in a higher probability of economic weakness.