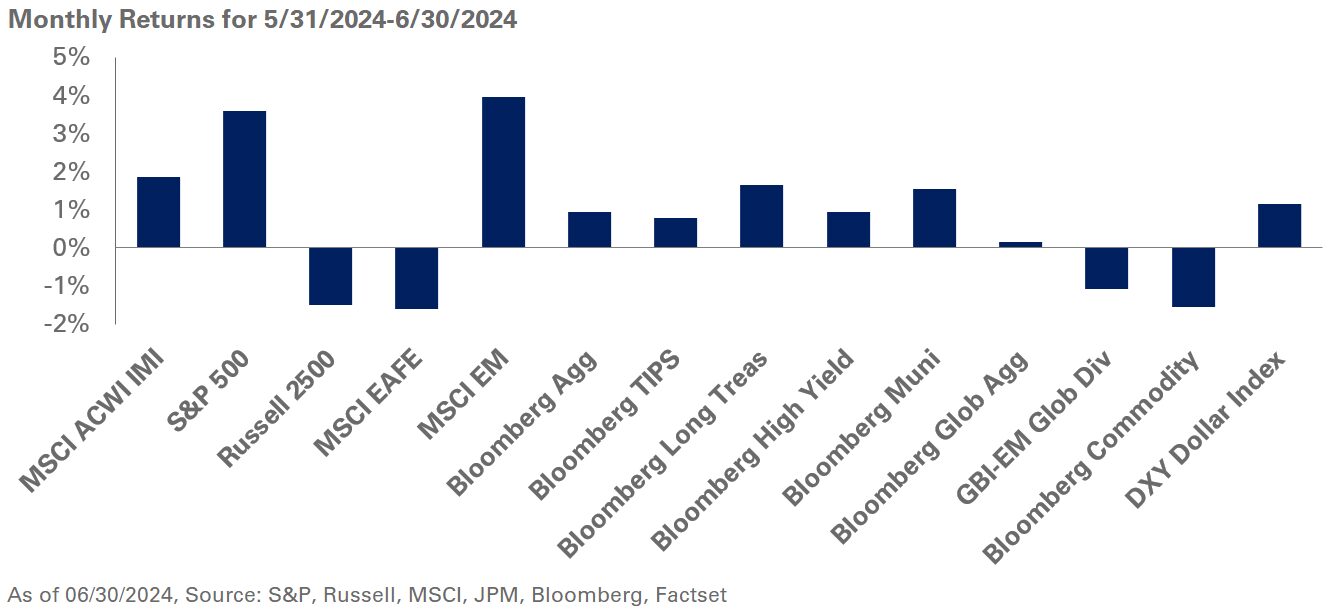

It was the same story but a different month for stocks in June, with growth outperforming value. The artificial intelligence (AI) boom within the tech sector appears unstoppable as Nvidia, the leading provider of chips used to run AI models and the primary benefactor, by far, of this boom, is now up over 150% year-to-date while briefly surpassing Microsoft as the largest publicly-listed U.S. company last month.

Large-cap growth stocks gained 6.7% in June and are now up over 20% so far this year. Meanwhile, large-cap value equities struggled last month, down 0.9%, and have returned 6.6% for the year. Overall, U.S. large-cap stocks were up 3.6% in June, with year-to-date gains totaling 15.3%, according to the S&P 500 Index. U.S. small-cap equities lagged in June, down 0.9%, up a modest 1.7% for the year, widening the performance gap between large- and small-cap U.S. stocks. Global equities gained 2.2% with EAFE stocks down 1.6% and emerging market equities up 3.9% in June.

On the macroeconomic front, key economic data is still showing a growing, but slowing U.S. economy with real GDP growth revised up to 1.4% in the first quarter, down from 3.4% in the fourth quarter of 2023. Inflation for May (reported in June) came in below expectations with headline inflation flat for the month and core inflation rising 0.2% during the same period. Finally, the jobs market is holding strong with data on weekly jobless claims and job openings exhibiting no weakness; however, the monthly jobs report for June showed the unemployment rate climbing to 4.1%. With the risk of another inflation flareup appearing to wane, markets will likely focus on jobs data for signs of a slowing economy.

The Federal Open Market Committee met in June and maintained the federal funds rate at 5.25%-5.50%, while affirming its dependence on data for future moves. The Committee’s median expectation for the policy rate at the end of 2024 changed, rising to 5.1% from 4.6% last surveyed in March. This shift was expected as the FOMC’s expectations for rate cuts this year have converged to the market’s expectation of one-to-two cuts in 2024.

Meanwhile, the two-year Treasury yield—a proxy for short-term market expectations for Fed interest rate policy—declined to 4.7% from 4.9% in June. During this period, long-bond yields were lower, with the 10-year at 4.4% and the 30-year at 4.5%. Credit markets showed strength with spread levels remaining tight and flat in June with investment-grade spreads at 94 basis points and high-yields spreads at 309 basis points. High-yield debt remains attractive, but we advocate caution entering at these spread levels.

Elsewhere, energy markets ended June higher with WTI Crude Oil spot prices up 7.6%, ending at $83 per barrel. Overall, the Bloomberg Commodity Index decreased 1.5% for the month.

We continue to recommend investors diversify their holdings of U.S. large-cap stocks with quality- and value-oriented exposures. Further, we believe global equity strategies remain compelling and encourage greater use of active equity approaches. We encourage the positioning of duration-neutral fixed income relative to strategic targets as we do not anticipate rates to move meaningfully higher from current levels. We also advocate investors add strategic exposure to U.S. TIPS given the current level of real interest rates and breakeven inflation levels.