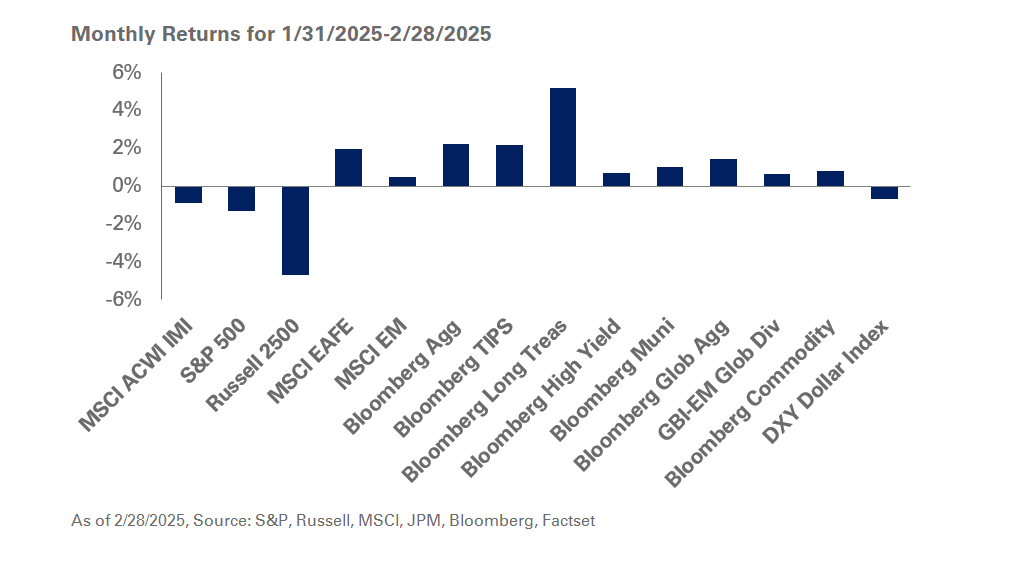

In another noisy month for markets, a flurry of headlines around potential policy changes from the Trump Administration fueled widespread uncertainty, weighing down sentiment and reigniting concerns around economic growth. As a result, U.S. equities underperformed their global counterparts and value equities outperformed growth stocks. Notably, the S&P 500 Index fell 1.3% in February, with the mega-cap names leading the declines. The Russell 1000 Value Index eked out a 0.4% gain for the month, while the Russell 1000 Growth fell 3.6% – wedging a further gap between the indexes on a year-to-date basis with the value index up 5.1%, while growth remains in the red with losses of 1.7% so far this year.

Outside the U.S., local returns were bolstered by a weaker dollar and improving economic data: the MSCI EAFE and MSCI Emerging Markets indexes gained 1.9% and 0.5%, respectively, last month. China was the best performing market—the MSCI China Index added 11.8% in February— as technology names continued to benefit from positive momentum following DeepSeek’s announcement earlier this year on the capabilities of its cost-efficient artificial intelligence models.

Escalating growth concerns fueled downward pressure in interest rates and gains across most fixed-income securities. In the U.S., yields fell across the curve, with 10- and 30-year Treasury yields falling 33 and 30 basis points, respectively. In response, longer-duration indexes outperformed last month with the Bloomberg Long Treasury Index gaining 5.2%. Within credit, option-adjusted spreads widened, particularly among lower-quality names. The spread on the Bloomberg U.S. High Yield Corporate Index increased 20 basis points to 280; however, this level still remains within long-term median spread levels. The spread widening weighed on credit indexes on a relative basis: the Bloomberg U.S. High Yield Corporate Index ended modestly higher, adding 0.7% in February.

Within real assets, spot gold prices extended recent gains, returning 2.2% last month, amid the supportive macroeconomic backdrop and demand for safe-haven assets. The commodity complex continues to see significant dispersion, with crude oil prices falling 4.3%, even as the Bloomberg Commodity Index increased 0.8%.

We encourage holding safe-haven fixed income at strategic targets as a buffer against economic downturns and market shocks. We remain steadfast in our recommendation to diversify S&P 500 exposure by complementing with value and quality factors to produce a balanced U.S. large-cap position. We encourage investors to remain disciplined and stick to long-term strategic asset allocation targets. At the same time, we urge our clients to keep liquidity on hand to rebalance should the market overreact to any unexpected headlines in the coming months.