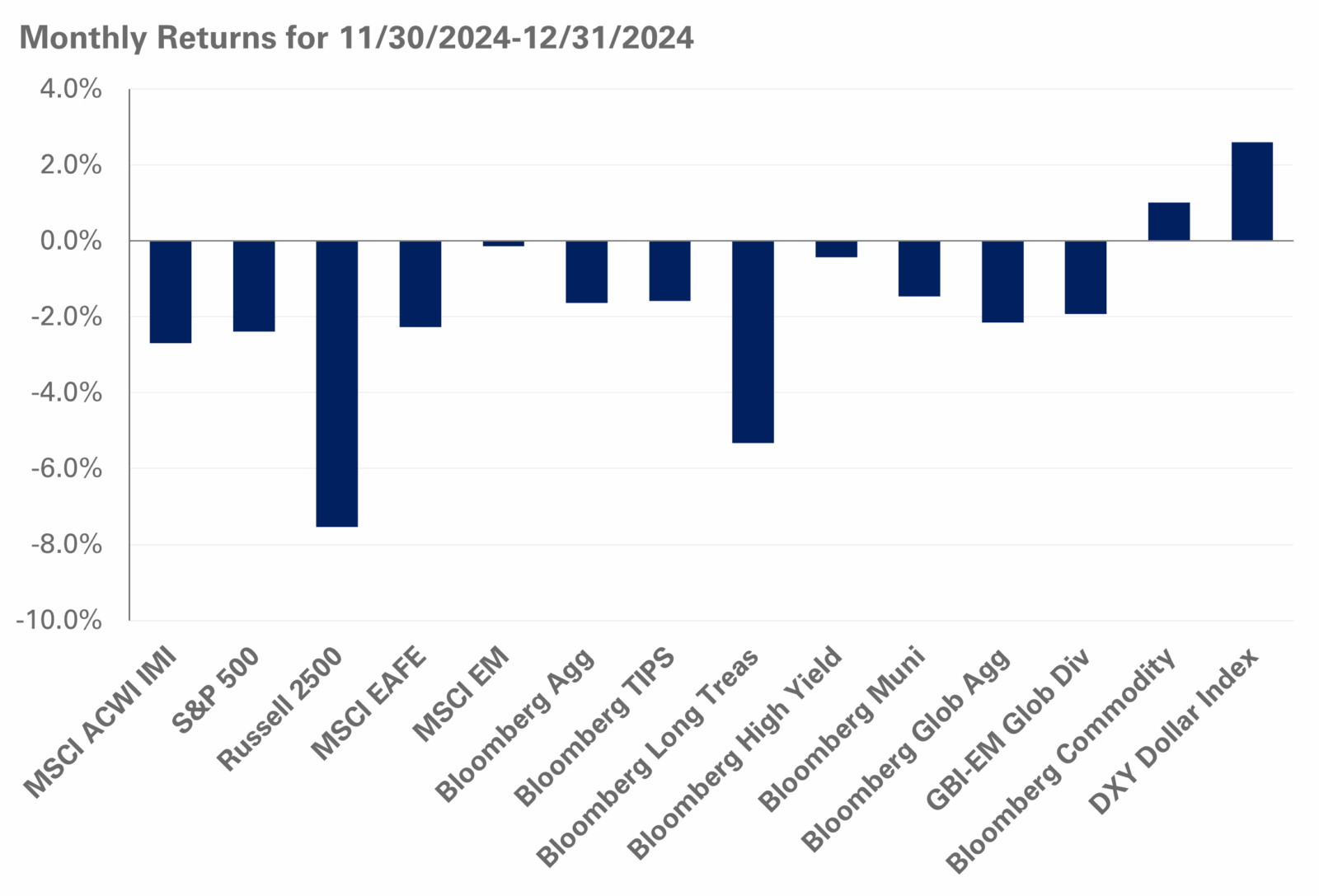

Markets ended the year with a whimper in December as post-election euphoria waned in the United States. Domestic equities finished the month down 2.4% with value stocks bearing the brunt of the losses with declines of 6.8%; meanwhile, growth stocks eked out gains of 0.9%. Small-cap equities continue to lag, falling 7.5% in December. Global equities fell 2.7% with the EAFE Index losing 2.3% and emerging markets down 0.1%.

Key economic data is still showing a growing U.S. economy with the final estimate for real GDP growth revised up to 3.1% for the third quarter from 3.0% in the prior quarter. Inflation for November (reported in December) met expectations with headline inflation rising 0.3% for the month, reflecting a 2.7% year-over-year increase. The jobs market is also holding strong with weekly jobless claims and job openings data showing no weakness; while recent monthly jobs reports have shown the unemployment rate increasing, the jobs report for November surprised markets with an addition of 227,000 jobs. As inflation moderates, jobs data will take center stage as the Federal Reserve pivots to focus on the labor market as part of the central bank’s dual mandate of stable prices and full employment.

The Federal Open Market Committee met in December and cut interest rates by 25 basis points to set the range of the federal funds rate to 4.25%-4.50%. The updated Fed dot plot survey of interest rate expectations shows two cuts of 25 basis points each in 2025, while pointing to expectations of an uptick in the long-run interest rate to 3%, a measure that has consistently risen from 2.5% in the beginning of 2024.

The two-year U.S. Treasury yield, a proxy for short-term market expectations for Fed interest rate policy, remained flat at 4.2% in December. However, long-bond yields rose sharply with the 10- and 30-year yields up 40 basis points to 4.6% and 4.8%, respectively. Credit markets continue to show strength with spread levels remaining tight with investment-grade spreads below 80 basis points and high-yields spreads under 300 basis points. At current spread levels and expectations for lower base rates moving forward, we suggest using high-yield bonds as a source of portfolio liquidity.

Energy markets finished the year higher with WTI Crude Oil spot prices rising 6.1% to $72/barrel. Downward pressure from metals offset gains from energy, leading to modest gains of 1% for commodities overall in December.

We encourage neutral duration positioning relative to strategic targets given the current interest rate environment. We remain steadfast in our recommendation to diversify U.S. equity exposure with a blend of S&P 500 and value exposures within U.S. large-cap stocks. We encourage investors to remain disciplined and stick to long-term strategic asset allocation targets. At the same time, we urge our clients to keep liquidity on hand to rebalance should the market overreact to any unexpected headlines in the coming months.