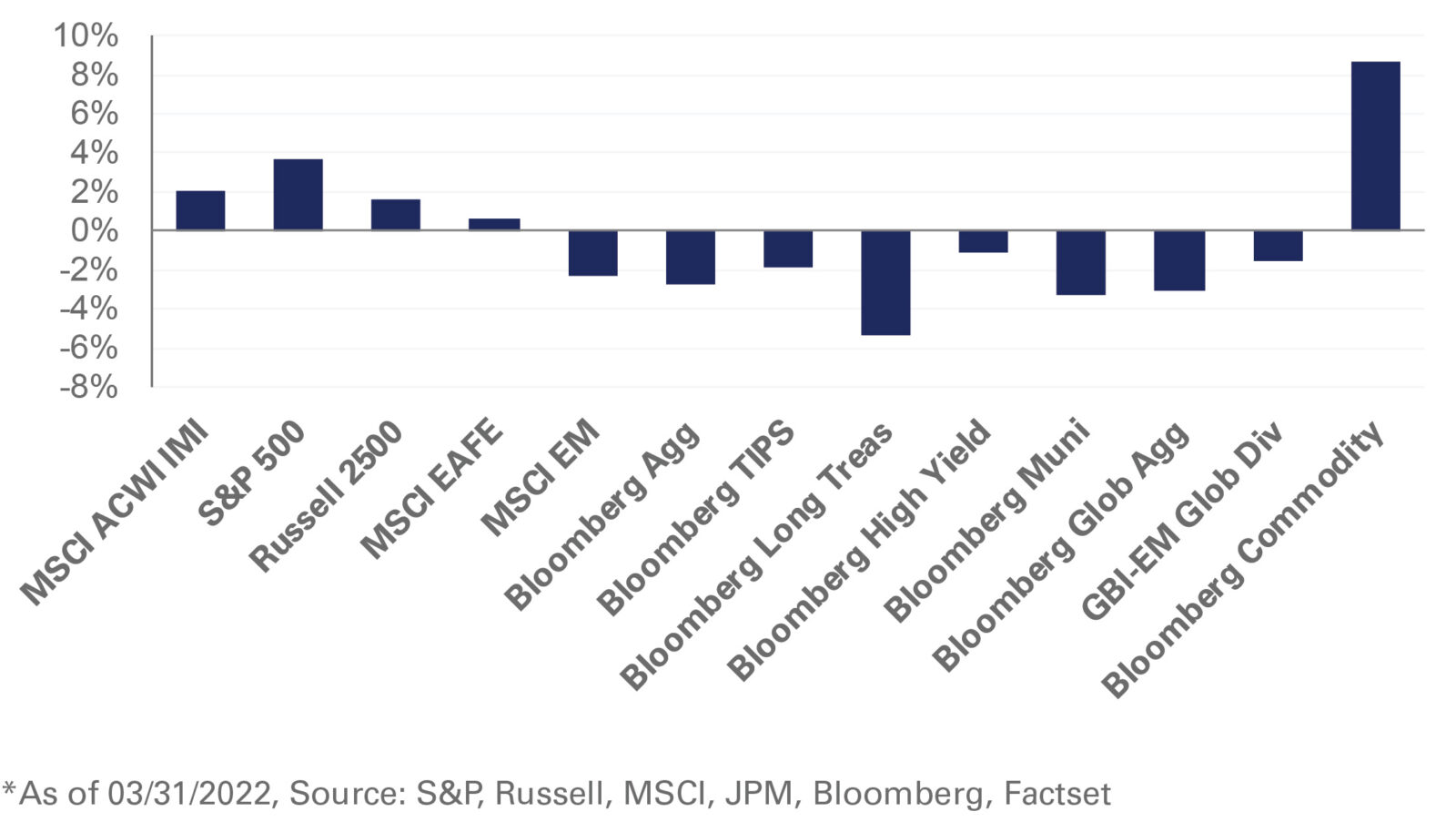

Ongoing geopolitical tensions and tighter monetary policy amid persisting inflationary pressures weighed on capital markets in March. The FOMC hiked rates for the first time since 2018, increasing interest rates by 25 basis points to a range of 0.25%-0.50%. Further, policymakers revised upwards their forecast for interest rates and inflation, and signaled for more aggressive monetary policy tightening to control inflation. As a result, market expectations for the number of Fed rate hikes in 2022 have increased to nine from five.

Despite these headwinds, the S&P 500 Index posted its first monthly gain in 2022, rising 3.7% and paring year-to-date losses to 4.6%. Non-U.S. developed equities were also in the black with the MSCI EAFE Index up 0.6% last month. Chinese equities lagged as market sentiment weakened due to geopolitical uncertainty and a surge in COVID-19 cases, which prompted lockdowns in parts of China. As a result, the MSCI Emerging Market and MSCI China indexes fell 2.3% and 8%, respectively.

In fixed income, the U.S. Treasury yield curve shifted higher due to expectations of tighter monetary conditions. The two- and 10-year Treasury yields increased 86 and 49 basis points, respectively, and the spread narrowed to four basis points. As a result, fixed-income assets broadly declined, while longer-duration assets underperformed: the Bloomberg Long Treasury Index fell 5.3% for the month. Further, inflation expectations continued to trend higher, with the 10-year breakeven inflation rate up 22 basis points to 2.8%. Despite higher inflation expectations, the Bloomberg U.S. TIPS Index fell 1.9% as higher real yields impacted prices.

Meanwhile, in real assets, the ongoing conflict between Ukraine and Russia continued to impact the global supply of commodities, pushing up prices. As a result, the Bloomberg Commodity Index gained 8.6% for the month.

NEPC’s stance towards risk assets has become more subdued given the more uncertain growth and inflation dynamics. As such, we continue to advocate adding value exposure to U.S. large-cap equity to help mitigate the portfolio impact of inflation normalizing above market expectations. Despite the recent hawkish shift from the Fed, we recommend investors maintain a dedicated allocation to assets that support liquidity needs in periods of stress.