Movements in Treasury rates, credit spreads, and asset returns yielded modest changes in funded ratios for many U.S. corporate pension plans in the first quarter of 2025. While domestic equities posted losses in the three months ended March 31, non-U.S. stocks were in the black during the same period. Total-return plans saw a modest decease in funded status as declines from return-seeking assets and Treasury rates offset gains from widening credit spreads. The LDI-focused plans experienced a modest rise due to their hedged position. Estimated discount rates for pension liabilities, based on long-duration fixed-income yields, decreased around six basis points for total-return plans and 12 basis points for LDI-focused plans in the third quarter. We estimate the funded status of our total-return plan fell about 0.4%, while funded status for our LDI-focused plan rose 0.8% during the same period.

Rate Movement Commentary

Short- and long-term interest rates decreased for the three months ended March 31. During the same period, the 30-year Treasury yield fell 19 basis points to 4.59%. In addition to the fall in yields, there was an increase of 17 basis points in long-credit spreads. In the first quarter, the drop in Treasury yields resulted in lower pension discount rates, with the discount rate for the open total-return plan falling six basis points to 5.60% and the discount rate for the frozen LDI-focused plan declining 12 basis points to 5.44% as of March 31.

Plan Sponsor Considerations

Non-U.S. stocks were generally positive in the first quarter, while domestic equities experienced losses due to market volatility and increased uncertainty surrounding tariffs imposed by the Trump administration. Investment-grade fixed-income markets posted gains across intermediate- and longer-dated maturities as yields moved lower. Performance of credit-oriented fixed-income assets was also positive as Treasury yields decreased and credit spreads widened. Total-return plans may want to consider the impact of rate volatility on plan liabilities and the role of LDI in light of the current rate environment. For certain plan sponsors, lower rates may increase liabilities and reduce funded status, which could lead to higher required contributions and PBGC variable-rate premiums. NEPC consultants are available to discuss the impact and cost of various pension finance and derisking strategies related to rate movements and volatility in the market.

Market Environment and Yield Curve Movement

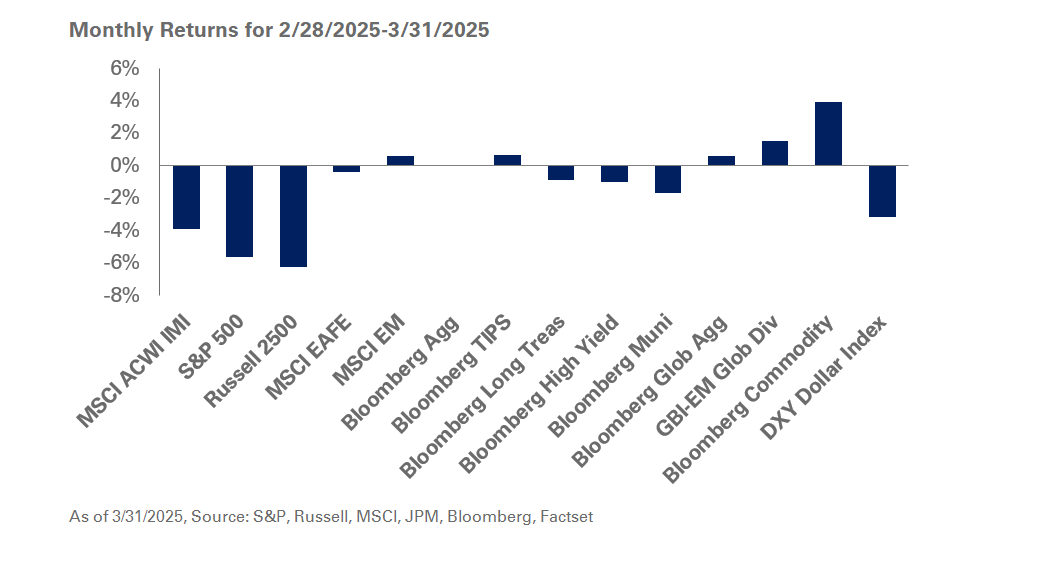

U.S. equities fell 4.3% in the first quarter. The MSCI EAFE increased 6.9% in the three months ended March 31; the MSCI Emerging Market Index rose 6.9% during the same period.

Treasury yields decreased and the yield curve remains inverted across only a few maturities. The 30-year Treasury yield fell 20-basis points in the first quarter, resulting in gains of 4.7% for the Bloomberg Long Treasury Index; during the same period, the Bloomberg Long Credit Index rose 2.5%.

Related Insights