Extension strategies are finding their place in the sun.

Often overlooked and underutilized, this investment approach offers an opportunity to generate alpha as investors come off a very lucrative two years and are now facing an uncertain market environment. At NEPC, we believe extension strategies are an effective tool in an investment landscape marked by increased market volatility, and index concentration as the S&P 500 weighting of the so-called Magnificent Seven—Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia and Tesla—hovers around 30% of the index. At the same time, we also believe it is necessary to fully understand the risks associated with extension strategies and thoroughly evaluate them.

Extension strategies are similar to their long-only counterparts, but they also possess the unique ability to short stocks, allowing them to benefit when stock prices move up AND down —a compelling feature when markets are beset by volatility. There are different kinds of extension strategies, typically defined by the magnitude of gross exposure, for instance, 130/30 or 150/50, with the first number reflecting the long exposure and the second describing its short exposure. Most extension strategies target a beta of 1 to their index, similar to most long-only peers.

This investment approach is becoming increasingly popular with investors because of its following benefits:

- Shorting: Relaxing the shorting constraint for extension strategies allows the manager to generate alpha across both its long and short books by fully expressing its views on each individual stock. Traditional actively managed long-only strategies are often limited by the extent of the underweight of a particular name based on that stock’s weight within the index. The ability to short allows extension strategies to more meaningfully underweight stocks that could potentially decrease in value over time. This unique feature to short is important because most of the constituents in benchmark indexes have fairly small index weights which potentially handcuff long-only managers from fully expressing a negative opinion on a stock.

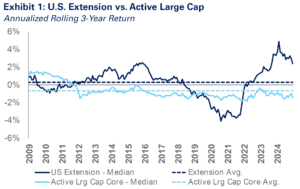

As of December 2024 Source: eVestment Conversely, the ability to use short proceeds also allows the manager to deploy those funds into higher-conviction long ideas. This results in a broader opportunity set and the ability to fully express views on both the long and short side, all while keeping the underlying capital commitment and beta similar to a long-only approach.

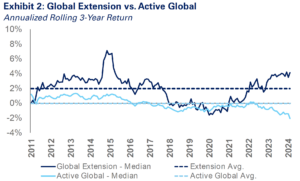

- Information ratio: High-quality extension strategies often exhibit a higher information ratio relative to their long-only peers. With an increased opportunity set and more flexibility, investors should expect better outcomes and higher efficiency for extension strategies relative to a long-only version of the same strategy. In Exhibit 1, we look at the rolling three-year excess returns for the median U.S. equity long-only strategy and the median U.S. equity extension strategy. We also broaden our analysis and perform a similar exercise on a global scale to see if there are any differences in our results

As of December 2024 Source: eVestment (Exhibit 2). Across both sets of analyses, we observe the median extension strategy (net of fees) generates an average rolling three-year return that is higher than its long-only counterpart.

- New macro environment:Hedge funds, more specifically extension strategies, have suffered over a decade’s worth of headwinds.However, many of those headwinds have flipped to tailwinds given the recent market volatility.Also, in our new higher-rate investment regime, the rebate earned for shorting has increased significantly, providing a boost to long/short strategies broadly. Last, but not least, index concentration risk in the U.S. remains a perplexing issue for investors. Extension strategies have greater flexibility to mitigate index concentration risk by underweighting potentially overvalued but heavily weighted names within the index.

While there are clear benefits to the structure and flexibility of extension strategies, investors should also be mindful of these potential risks and how best to evaluate them:

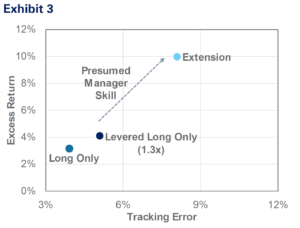

- Leverage: Any implementation approach that includes shorting introduces leverage into the equation which investors should be mindful of. For example, a 130/30 extension strategy has a gross exposure of 160% or, put another way, 1.6x the leverage of the long-only version of the strategy. While not all leverage is bad, it is critical to understand it in relation to extension strategies. It is our belief that employing leverage is not a skill worth paying for in isolation. As a result, the evaluation of extension strategies should include determining how much outperformance (relative to long-only) stems from pure leverage versus manager skill; please see Exhibit 3 depicting these components of performance.

- Manager skill and framework: Not all managers can efficiently forecast positive and negative stock returns; traditional managers have historically relied on an investment process designed to take each stock within a benchmark and reduce it to a universe of names that are more feasible for in-depth research. This process is designed to enable the manager to find stocks that will likely increase in value over time; assuming managers can solely rely on the inverse of this process to find attractive short positions is simplistic and naïve. The process and resources around generating short ideas tends to be a unique skill set as proven by the challenges of long/short hedge funds over the past several years. In addition, it is also important to consider the sophisticated and complex investment, legal and operational infrastructure needed to short.

- Fees: Investors continue to wrestle with the fees associated with extension strategies. The fee structures can range from flat management fees to performance-based fees. Performance-based fees, which include a base management fee and an incentive fee on profits over a specified benchmark, have become popular over the years. We believe a performance-based fee structure further aligns our clients’ incentives with that of the manager. Under this format, the management fee is typically significantly lower than an active long-only manager in times of underperformance and considerably higher when the manager outperforms, with investors more inclined to pay for value addition.

The difference in these structures can be meaningful given the challenges active managers have faced adding significant value in an efficient market. For example, the average rolling one-year excess (gross) return of the median active large-cap equity manager is 0.35%. When you strip out the median fee within that same universe of 0.50%, it is easy to understand the frustration of investors paying more in fees than alpha generated. Extension strategies with appropriately negotiated performance-based fees help investors mitigate this dynamic. That said, many investors find it challenging to not fully know how much in fees they may pay in a given year within a performance-based fee structure, which may carry implications even outside of their investment programs.

At NEPC, we believe extension strategies—often times underrepresented in client portfolios—can be an effective tool to generate alpha while keeping some of the similar constructs of long-only investing. We understand how to assess, select and implement these investment strategies. We know not all managers are created equal; it is necessary to evaluate each extension strategy based on its individual strengths and weaknesses, while accounting for every investor’s unique set of risk tolerance and return requirements. To that end, we harness a proprietary framework to assess the historical performance of a manager’s extension strategy versus its long-only version, their ability and infrastructure to generate short alpha, the percentage of extension alpha that is eroded by the higher fee profile of extension strategies, and the efficiency of their approach.

We invite you to partner with NEPC’s Investment Team to better understand if extension strategies are a suitable fit for your specific investment programs. Please reach out to your NEPC consultant to learn more or for any questions you may have.