This is the third installment in a multi-part series on portfolio construction for insurance general accounts. In this edition, we focus on optimizing public equity portfolios. It follows our earlier pieces on building and implementing allocations to private markets and opportunistic credit.

Insurers should take a closer look at their public equity allocations.

High volatility and capital charges often limit the size of an insurer’s public equity holdings. As a result, insurance companies should pay special attention to their equity exposures to ensure they are optimizing the returns and risk of an asset class that can provide upside potential and be accessed cheaply and efficiently.

At NEPC, we believe there can be material differences in performance depending on how you invest in equities. These differences can arise from the size of the target allocation, the regional and sector exposure, implementation, manager and vehicle selection, and benchmarking. We encourage insurance companies to review the objectives and contents of their public equity allocations to potentially improve outcomes.

Sizing Target Allocations

In general, asset allocations will vary across organizations, driven by an insurer’s surplus position, risk tolerance, and business lines. Life insurance companies, for example, typically allocate very little capital to public equities largely because of the high capital charges they carry. Where possible, we suggest a minimum target allocation of 5% so that the allocation can have an impact on the total portfolio.

For property and casualty and health insurance companies, public equity allocations can extend upwards of 30% of total portfolio assets, but typically reside in the 15%-to-20% range. As we describe below, the type of public equity exposure and the size of the target allocation often go hand-in-hand. Insurers that own value or defensive equities might be able to tolerate a higher allocation, while those with more growth or emerging market exposure might prefer a smaller target allocation. As always, we recommend performing a detailed asset allocation study to determine an appropriate target allocation.

Exposure to Regions and Market Capitalizations

Our long-term strategic view for our investors is to utilize the MSCI All Country World Investable Market Index (MSCI ACWI IMI) as the strategic asset allocation target and investment policy benchmark for public equity. This benchmark offers a broad representation of the global investable opportunity set, including stocks of small-cap companies. From a regional perspective, this benchmark is roughly 65% U.S., 25% non-U.S. developed, and 10% emerging markets equities.

While the MSCI ACWI IMI may be appropriate for general account portfolios with larger allocations to public equities, we believe modest adjustments can be made to accommodate portfolios with smaller target allocations; notably, removing small-cap and emerging market exposure can result in a less volatile exposure. The appropriate starting point in this case would be the MSCI World Index which is approximately 75% U.S., and 25% non-U.S. developed equities, and includes only large- and mid-cap companies.

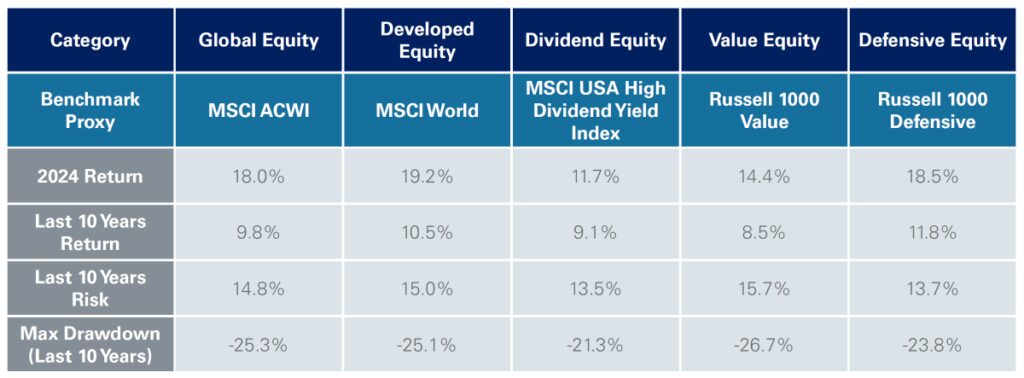

In some cases, insurance investors will want to take an additional step and focus exclusively on U.S. large-cap equity to further simplify their exposure. Other modifications can include focusing on high- dividend-paying or so-called defensive stocks to enhance income and/or reduce volatility. Importantly, we caution insurers to avoid thinking of these exposures interchangeably. As shown in the table below, return and risk outcomes can vary widely across different benchmarks that are often thought to be similar (e.g., value, dividend, defensive equities). The selection of a benchmark/ exposure should be done in tandem with setting the public equity strategic target allocation.

Active Versus Passive

At NEPC, we generally prefer active approaches in less efficient asset classes such as small-cap and international equities. More efficient asset classes, such as U.S. large-cap stocks, are better candidates for passive mandates. While this is also true for insurance companies, we believe insurance investors should consider additional characteristics of individual mandates when deciding between active and passive. For example, portfolio turnover and tracking error are other metrics which should be reviewed before implementing a strategy.

Specifically, active approaches that have high levels of turnover may result in higher levels of realized gains or losses. Similarly, strategies which are more concentrated may have higher tracking error and potentially greater risk overall. For these reasons, we have a bias towards passively managed equity mandates within insurance general account portfolios; active approaches can and should be considered, but understanding the strategy’s trading frequencies and overall risk level are important when deciding between strategies.

Tax Considerations

Investors looking to avoid purely passive mandates may want to consider tax-optimized strategies that incorporate an insurer’s preference on gains and losses. Tax optimized strategies involve loss harvesting that can result in tax alpha that potentially improves after-tax performance. The extent of tax savings from loss harvesting will vary depending on the type of market and the portfolio’s guidelines.

These strategies offer a nice middle ground between pure passive mandates and higher turnover active strategies. Guidelines and benchmarks can often be customized, and insurers can provide a gain/loss budget to the asset manager that is used when rotating the portfolio. The portfolio managers can also operate on a net-zero basis whereby gains and losses are offset, resulting in no tax impact to the insurer.

As with many other exposures, we prefer to implement these strategies with asset managers that have familiarity managing assets for insurance companies. Setting appropriate benchmarks and guidelines should be done at the outset of the mandate.

Vehicle Selection

Many insurance investors prefer to utilize separate accounts primarily due to better flexibility/ control over underlying holdings or, in the case of fixed-income mandates, more favorable capital treatment. Within public equities, we find that insurers utilize a wider range of vehicles. Mutual funds and exchange-traded funds may be appropriate for investors with smaller allocations or when accessing more complex markets, for instance, small-cap or international equities.

We typically find separate accounts being used for U.S. large-cap stocks. In some cases, insurance investors may want to take advantage of the tax optimized approach we described earlier or perhaps build a more customized exposure (such as defensive or high-dividend paying equities). In these cases, a custom separate account may be appropriate.

As the capital charges are the same across vehicles within public equities, we are somewhat agnostic. Of course, fees are among the many factors that should be considered when selecting a vehicle.

To learn more about constructing and implementing investment portfolios for insurance general accounts, or to conduct asset allocation and enterprise risk management studies to determine an appropriate public equity target allocation for your portfolio, please contact your NEPC consultant.