Smaller continued to be better for higher educational endowments in the fiscal year ending June 30, 2024 (mega endowments are those with greater than $1 billion in assets under management, or AUM, as tracked by NEPC at the time of writing). Results were strong for nearly all higher educational endowments, but for the second year in a row, the largest endowments generally trailed behind their smaller counterparts.

The trend reflects dramatic gains for the public equity markets during the year. As we have noted over the years, these mega endowments typically carry greater allocations to private equity and venture capital, compared with their smaller counterparts. Historically, private investment opportunities have provided a performance edge to these larger institutions, with the strongest returns accruing to endowments that could access the top capacity-constrained managers.

Since late 2022, however, public large-cap equities in the US have been the performance leaders, spurred by exceptional gains for large technology corporations at the forefront of the artificial intelligence revolution. This trend has been of great value to smaller and mid-sized endowments with higher US large-cap exposure.

Artificial Intelligence, Real Gains

Artificial intelligence-related products and services exploded in the past fiscal year, quickly transforming the outlook for business processes globally. They also provided extraordinary acceleration in earnings and growth expectations for the US firms that are leading the AI market.

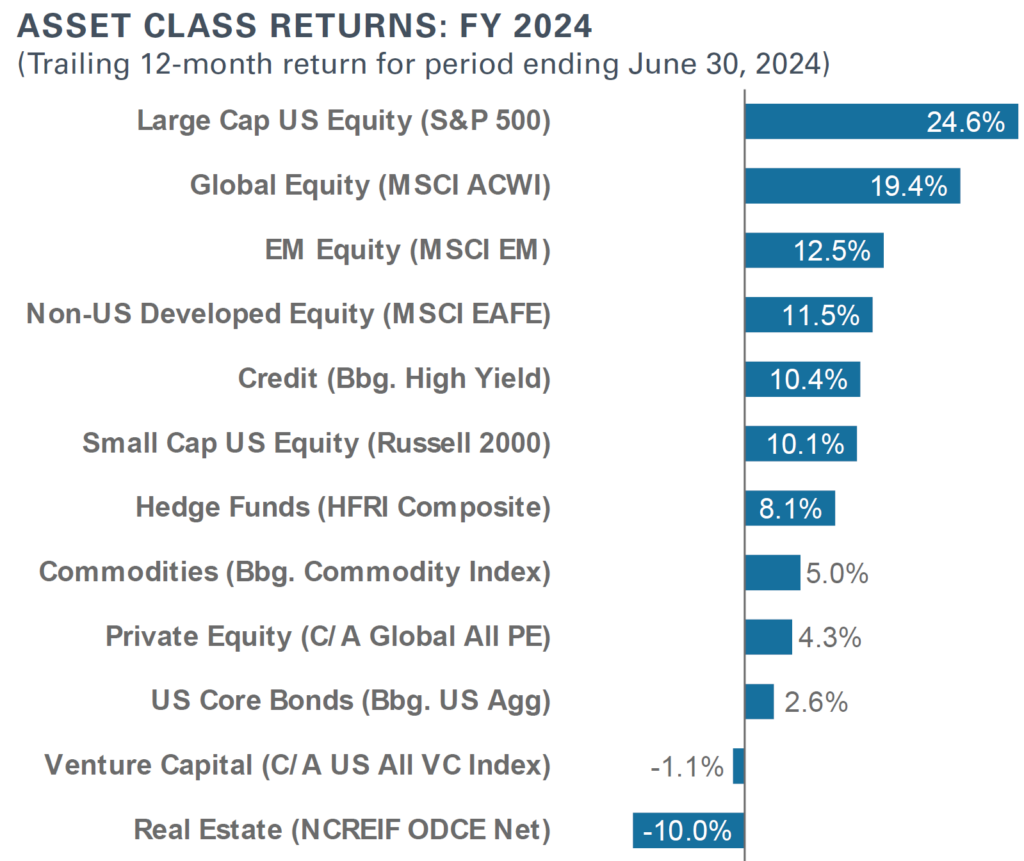

It’s often true that compelling new technologies arise in the private markets first, which is a key reason why the mega endowments have historically outperformed. In this case, the AI leaders are mainly established, U.S. domiciled public-market tech firms, like Nvidia, Amazon, and Microsoft. These companies helped drive gains of 24.6% for the S&P 500.

Their success has been a powerful boon to the average- or smaller-scale endowments that tend to have much more exposure to public equities. According the latest NACUBO-Commonfund Study of Endowments, higher educational endowments with between $100-250 million in AUM – where the median foundation lands – had nearly 30% invested in US public equities, compared with 15% for endowments with $1-5 billion in AUM, and significantly higher than the 8% held by endowments with more than $5 billion in AUM.

In like fashion, mega endowments tend to have meaningfully higher allocations to private markets, which broadly lagged. NACUBO data shows the largest endowments – those with more than $5 billion in AUM – have 14% of assets allocated to venture capital and 20% to other private equity investments. Meanwhile, endowments in the $100-250 million had only 3% and 8% in these respective asset classes.

While private equity exposures produced largely positive results for mega endowments, they were not at the same scale as the US public market. Venture capital allocations were a net negative, as the sector continued to adapt to a higher-interest-rate, higher-cost-of-capital environment.

More broadly, the US economy benefited from some moderation in the inflation rate, which has reduced pressure on the Federal Reserve to keep interest rates up. Growing expectations for renewed interest rate cuts and some spread compression were beneficial for public financial markets as well, providing further fuel for equity and fixed income returns during the fiscal year.

Top Performer Highlights

The University of California-San Diego Foundation (UC San Diego) remained the top performer among mega endowments for the second fiscal year in a row in 2024. At 15.5%, its results significantly outpaced the median mega endowment return of 10.5% (as measured by this report).

The Foundation’s success stems from a unique approach to endowment management that is a particularly good fit for current market trends. They utilize several University of California General Endowment Pool accounts, enhancing them with their own strategic position which consists primarily of U.S. large-cap equity. It’s a hybrid approach that allows them to benefit from the University of California Investment Office’s resources while employing an asset allocation that meets their own needs.

Their returns for the most recent year were driven by a decision to have a meaningfully higher allocation to public equity than many of their large endowment peers – specifically to US large-cap – via low-cost passive strategies. Public market equity accounted for just over 60% of the total portfolio weight and drove approximately 90% of the fund’s total returns for the year.

Another top performer in the last two years has been the University of Miami. Asaf Zentler, Interim Chief Investments Officer & Treasurer for the University endowment, has indicated that public market exposure played a key role. “The University of Miami’s one-year performance was largely attributed to its relatively high allocation to public equities,” noted Zentler in a recent interview. “They accounted for approximately 65% of the portfolio but contributed about 85% of the total returns during the year.”

Looking Forward

The success of AI has driven outsized gains for smaller endowments with high exposure to large-cap US public equities, but we’re not convinced this is a trend with staying power. While AI leaders have generated significant earnings growth, their stock-price gains also benefited from higher valuation multiples. It may be difficult for them to outperform already rosy earnings expectations to support the current high price-to-earnings multiples going forward.

We also believe that private equity and venture capital aren’t likely to remain underperforming sectors for an extended period of time. Both segments needed to endure a period of repricing in an environment of higher interest rates, but we think that cycle will come to an end now that interest rates are expected to remain stable or come down.

Private equity and venture capital have a higher risk/reward profile than public equities, and historically they have provided the widest range of investment opportunities. We believe innovation will continue to occur and those financing it will be rewarded. Rather than avoiding private equity and venture capital, we advise clients to approach those sectors with a disciplined, diversified approach, sticking to their strategic targets and annual pacing plans.

Indeed, this year’s trends reinforce the importance of diversification in endowment portfolios. The ideal endowment portfolio targets some form of spending-plus-inflation return, with limited volatility. Diversification with a long-term vision are excellent tools to achieve those goals, even though the performance of various asset classes may ebb and flow over time.

NEPC classifies a “Mega Endowment” as any endowment that meets or exceeds $1B in assets. Information for this report was gathered by analyzing publicly available data and public news releases that have been published prior to December 31, 2024. NEPC’s Mega Endowment list does not reflect data from institutions that do not provide readily available public returns, have not published their data prior to NEPC’s cutoff date, or do not meet or exceed the $1B threshold based on the 2023 NACUBO Report or prior versions of this list.