The recent market turmoil has emphasized the need for one of the top portfolio construction disciplines – “Diversification”. While many investors utilize a mix of strategies to create a diversifying allocation, we believe that the optimal approach should have two main characteristics: 1) provide complementary attributes in various market environments and 2) include strategies with a low correlation to each other and a portfolio consisting of stocks, bonds, and private investments. These approaches—often overlooked in an upmarket—help diversify away from equity risk which is the most prevalent risk in investment portfolios. They also help stabilize the portfolio over the long term and improve risk-adjusted returns. Diversifying strategies are diversifying to stocks, bonds, and private investments because their exposures are different. More importantly, the most diversifying strategies utilize investment processes that produce returns driven by idiosyncratic risk rather than factor risk.

A portfolio assembled with complementary diversifying approaches will produce a more stable return than one more narrowly allocated in fewer strategies that tend to only perform well in specific market conditions. At NEPC, we think it is critical to establish clear goals and expectations when building a diversifying allocation. In our view, a diversifying allocation is meant to complete portfolio construction, not compete with the return-seeking portion of the total portfolio.

The paper below was originally published in December 2024.

Investors can count on a broad array of strategies to incorporate diversification into their portfolios.

These approaches—often overlooked in an upmarket—help diversify away from equity risk which is the most prevalent risk in investment portfolios. They also help stabilize the portfolio over the long term and improve risk-adjusted returns. Gains originating from diversifying strategies can serve as a source of liquidity during/post a market downturn, serve as dry powder to reinvest following periods of stress, reduce volatility drag, and/or increase the terminal value of the portfolio.

At NEPC, we think it is critical to establish clear goals and expectations when building a diversifying allocation. If investors are unclear on the goals of the allocation, they are more likely to abandon the strategy. In our view, a diversifying allocation is meant to complete portfolio construction, not compete with the return-seeking portion of the total portfolio.

While many investors utilize a mix of strategies to create a diversifying allocation, we believe that the optimal approach should have two main characteristics: provide complementary attributes in various market environments and include strategies with a low correlation to each other and a portfolio consisting of stocks, bonds, and private investments. As a result, in this paper, we focus on global macro and trend following, fund-of-hedge-funds, multi-strategy, and event-driven approaches.

We believe that when these five low-correlated approaches are combined and customized to meet the individual investment goals of our clients, they can efficiently achieve the required level of diversification while earning returns over a full market cycle.

1. What are Diversifying Strategies?

Diversifying strategies (“DS”) provide diversification to the rest of an investment portfolio through the types of exposures they offer along with the specific strategies utilized to generate returns. DS typically have multi-asset and multi-regional exposures which intrinsically provide diversification of risk factors to a portfolio with stocks, bonds and private investments. For example, some DS have exposures to areas of the market such as commodities and currencies that are driven by different fundamentals than equities or fixed income.

The implementation of trading strategies can create additional diversification, for instance, some approaches can short exposures elsewhere in their portfolio, while others can isolate idiosyncratic exposures through hedging.

2. Why Diversifying Strategies Matter

Investors take varying levels of desired risk based on a range of factors, including the profile of their liabilities, behavioral sensitivities to drawdowns, and time-horizon. Thanks to their uncorrelated/low correlation profile versus bonds and stocks, DS aim to improve the overall portfolio’s stability allowing investors to limit the frequency and/or magnitude of drawdowns and improve performance consistency.

For investors with significant liabilities, such as defined benefit pension plans, DS can help buffer funding ratio volatility and honor distributions during periods of market stress through the monetization of gains originating from the risk-mitigating portion of their portfolios. DS can also benefit less liability-sensitive investors, including endowments and foundations. These investors can utilize DS as a funding source to funnel into areas of opportunity during market drawdowns.

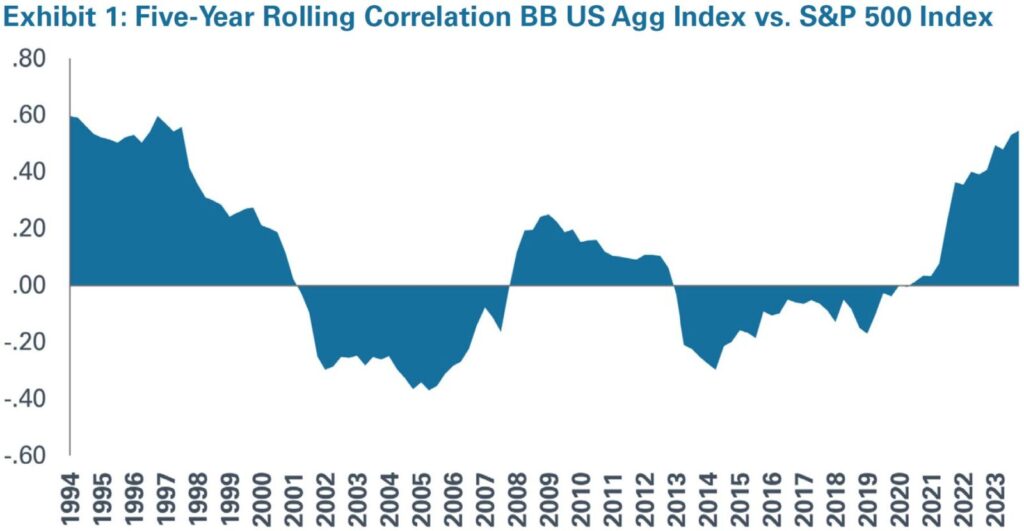

To be sure, fixed income could play similar roles, but it is important to keep in mind that stock/bond correlation has not been predictable historically, especially in a rising yield and/or inflationary environment. As recently as 2022, bond and equity markets sold off, while many DS, such as multi-strategy, macro, and trend following, emerged as winners.

In the prior decade, stock-bond correlation had mostly been negative, while in the decade before 2001 this correlation was positive. Exhibit 1 shows the changing pattern of the rolling correlation of bonds versus equities (as proxied by the Bloomberg Barclays US Aggregate, and S&P 500 indexes, respectively) going back to the early 1990s.

Traditional portfolio construction, that is, the typical 60/40 allocation model, can aggregate similar/related risk factors across seemingly different asset classes, exposing portfolios to undetected vulnerabilities that can get compounded at exactly the wrong time (often during periods of market stress). For example, high-yield and equity allocations can overexpose the portfolio to the closely related equity and credit factors.

Moreover, the contribution of risk in a 60/40 portfolio is driven primarily by equities, so the inclusion of DS allows for the portfolio to produce a more stable return across a range of market environments, aside from the strong growth, low-inflationary periods that have been best for equity performance.

Thanks to their uncorrelated alpha return characteristics, the right mix of DS should enhance the overall resiliency across a wider set of environments by decreasing the probability (and/or impact) of tail-risk-type market events. Therefore, the diversification of risk factors that DS provide can benefit a wide range of investors.

An essential feature of a portfolio with DS is its appealing liquidity structure. Many of the DS highlighted in this paper offer liquidity terms anywhere from daily to quarterly. Thus, this liquidity profile allows investors to rebalance capital into asset classes that have become more attractively valued due to changing market conditions. The ability to monetize gains during drawdowns also protects investors from having to source liquidity from the worst-affected parts of the portfolio.

The ultimate goal of DS is to improve the stability and risk-adjusted performance of the overall portfolio through their volatility dampening effect at the total portfolio level. Importantly, the reduced volatility drain increases the terminal value of the portfolio.

3. The NEPC Way

At NEPC, we believe an allocation to DS should have these key attributes within the context of a total portfolio:

- Low correlation and beta versus a stock-bond 60/40 portfolio

- Offer diversification of risk factors

- Provide complementary attributes in various market environments

- Serve as a funding source for liabilities and opportunities during market drawdowns

It is important to utilize strategies that are complementary to each other in terms of their ability to perform well in various market environments. A portfolio assembled with complementary diversifying approaches will produce a more stable return than one more narrowly allocated in fewer strategies that tend to only perform well in specific market conditions.

As a result, we chose to focus on the following core approaches: global macro, trend following, fund-of-hedge-funds, multi-strategy, and event-driven.

We think that by combining these five low-correlated approaches, most clients could efficiently achieve their specific target level of diversification while garnering a positive return over a full market cycle. Allocating across this set of core DS offers appealing characteristics such as low-to-moderate correlation and low-to-negative downside capture to a 60/40 blended portfolio. These characteristics, in turn, can help a given portfolio achieve a more consistent risk/return profile while offsetting existing equity/bond risk.

4. Core Diversifying Strategies

Global macro strategies are diversifying because they can capitalize on volatile market conditions, including periods when there are heightened geopolitical risks and/or more dispersion globally across rates, points on the yield curve, and/or commodity prices. Global macro strategies are long volatility and can help an investor efficiently diversify equity risk, as equities can struggle in volatile environments. Due to global macro’s typical distribution of returns, that is, its positive skew return profile, investors should expect relatively small gains/losses in most periods and large (but fewer) gains during times of market drawdowns. Global Macro can add protection to investor portfolios in volatile market environments and has performed well in times of stress. An investor who is predominantly interested in introducing a strongly uncorrelated return stream to their portfolio should consider allocating to global macro.

Trend-following systematic strategies aim to identify and capture persistent price-based—up and down—trends spanning various markets across fixed income, equities, commodities and currencies. Trend-followers are divergent by nature as opposed to most strategies that are inherently betting on positions converging to a particular value based on fundamentals and/or mean reversion. Therefore, these approaches benefit from trending prices, including extreme and/or idiosyncratic trends, irrespective of valuation rationale — this feature complements other strategies within the portfolio.

Event-driven strategies are core hedge fund allocations that blend return-seeking exposure with diversification to risk factors. While portfolios consist of mainly equities and credit securities, positions are held with the expectation of a catalyst materializing. These catalysts are generally unique to the specific company or issuer and, therefore, are less broadly correlated to the market. That said, correlations and betas will still be higher than the other diversifying strategies outlined in this paper; however, an allocation to event-driven will generally result in higher upside market capture, while keeping volatility significantly below that of equities.

Event-driven funds are opportunistic and can include sub-strategies such as: stressed/distressed debt, merger/risk arbitrage and activist investing. The strategy, as a whole, is fundamentals-based, taking advantage of mispricing, in which value is realized upon a catalyst event occurring, for instance, a refinancing, bankruptcy, litigation or spinoff. In certain economic environments, opportunities may favor one sub-strategy over another; however, allocations across these sub-strategies provide a continuum of opportunities spanning most economic environments. For example, during economic slowdown and recession, there is usually an increase in bankruptcies, liquidations and litigations, which is an ideal time for distressed investing, and is countercyclical with the market. Economic recovery and expansion are usually the peak time for industry consolidation, mergers and acquisitions and capital restructuring, which provides a strong investing environment for merger/risk arbitrage and activist approaches.

Multi-strategy direct and multi-strategy hedge-fund-of-funds can generate a lowly-correlated, all-weather return profile due to the diversity of the underlying strategies, including long/short, global macro, event-driven, commodities, systematic equities and volatility arbitrage. Some strategies perform well in supportive conditions for the market, such as more directional long/short equity and credit-focused strategies, or certain event-driven strategies, as mentioned above.

Other types of strategies perform well in environments with increased volatility, including global macro and volatility arbitrage strategies. Volatility arbitrage strategies are implemented in different ways, for instance, through dispersion trading which focuses on structuring trades that are long single stock volatility and short index volatility — a dislocation that exists due to the high utilization of hedges at the index level, but a relatively lower utilization of single stock hedges.

Other strategies included in multi-strategy products are minimally impacted by the economic environment, such as reinsurance strategies and statistical arbitrage. Statistical arbitrage employs a highly systematic approach towards trading on relative mispricing between stocks by neutralizing factor exposure: long/short many stocks within the same industry groups. These strategies are high-turnover, trading on signals using advanced techniques such as natural language processing, which explores the relationship between stock price movements and the type of words utilized by a CEO on an earnings call, that is, positive words such as growing, expansion and strength, or negative words such as declining, weakening and softening.

Together, these examples illustrate how DS can generate returns that are differentiated from the rest of the investment portfolio. While there is some overlap in the conditions that are beneficial to these strategies, these strategies largely target different inefficiencies making them complementary to one another.

5. Portfolio Considerations for Diversifying Strategies

Portfolio Interactions

Investors should consider the composition of the rest of their portfolio when determining the proper mix of diversifying strategies to select. There are a wide range of underlying strategies utilized in DS, with varying levels of diversification, risks and return-seeking attributes.

DS can be used as a plug to help investors create an overall portfolio that is more resilient across a range of market environments. Clients should think about the sensitivities of their overall portfolio to growth and inflation, along with other risk factors, when constructing a mix of DS that will help create a more balanced return profile across various economic regimes.

There is a high degree of customization that can be achieved in risk sensitivity that DS can help to mitigate. While asset classes generally exhibit sensitivity to growth and inflation, the most diversifying strategies show little, or even negative, correlation to these, which can help investors achieve a more consistent level of returns at the portfolio level. Some of these strategies can produce positive returns in environments that negatively impact equities, fixed income, or both simultaneously.

Many investors have a disproportionate concentration of risk in their portfolios driven by public and private equities which thrive in a high-growth, low-inflation environment. DS can help those keen on mitigating the portfolio’s overall reliance on this market environment. Other investors may be interested in taking on more risk in their DS portfolio due to a longer time horizon, weaker funded status in the case of defined benefit plans, or other factors that increase overall risk tolerance. As a result, these clients may be interested in implementing more return-seeking DS.

Underlying Strategy Considerations

An important distinction to consider in DS is whether the strategies are more directional or relative value in nature. Broadly, approaches that generate profits and losses utilizing relative value trade structures are more diversifying than strategies that take on more directional risk. One exception to this relationship are trend-following strategies that actively take long and short directional positions, based on identifying the strength of up or down price-based trends across a wide spectrum of distinct markets.

To illustrate this point, consider a directionally focused global macro strategy that takes views on the direction of interest rates. If the manager believes that interest rates are going to go down, they would be inclined to be long Treasuries, which is a view that would overlap with the rest of an investor’s long fixed-income exposure elsewhere in the portfolio. Other, more relative-value global-macro strategies prefer to avoid, or reduce, this duration risk by expressing views regarding the relative cheapness or richness between points on the yield curve (sometimes of a particular country and/or across a set of countries), for example, a two-year bond relative to a 10-year bond. This type of trade, which is often structured as a long position in one bond on the yield curve and short another, is less correlated to directional interest rates and price movements of fixed income.

Consider various implementations of equity long/short, an underlying strategy held in many multi-strategy hedge funds or offered as a standalone fund. Some equity long/short strategies—called market-neutral—construct portfolios that remove equity beta by having little net exposure, meaning long and short positions are sized similarly; they even remove differences in the risk factor composition of the long and short positions, so the overall portfolio has little exposure to non-idiosyncratic risk factors, including, size, style and sector. Other equity long/short strategies will allow higher net exposure and won’t hedge away as many non-idiosyncratic risk factors. As a result, these strategies are less diversifying to an investor’s portfolio, as these approaches will have some overlapping factor risk with the other assets that clients own.

Less hedged, more directional strategies with higher beta can have a role in DS portfolios as well, but their inclusion requires the investor to be thoughtful about assembling them in a way that directional exposures don’t build up, leaving the investor significantly exposed to a few risk factors. For instance, 2022 serves as a reminder of what can happen to hedge fund strategies that take on high levels of directional risk to the growth factor, as many of these strategies suffered significant losses that year.

Overall, we typically avoid recommending strategies for diversification purposes that come with hedge fund fee structures and have high components of beta in their return stream, as we advise clients to utilize higher cost-diversifying strategies for alpha and seek cheaper beta exposure elsewhere in their portfolios.

Below are some considerations at the strategy level for investors implementing a DS allocation:

a) Global Macro and Trend Following

Global macro strategies exhibit strong diversifying characteristics, including significantly lower volatility and downside risk compared to equities, lower drawdown profile versus both equities and bonds, positive skew (larger right tail) which complements equities’ negative skew, and a near-zero average correlation versus a 60/40 portfolio. Due to global macro’s typical distribution of returns (positive skew return profile), investors should expect relatively small gains/losses in most periods and large (albeit fewer) gains during times of market drawdowns. Global Macro can add protection to investment portfolios in volatile market environments and has performed well in past downturns.

Related to global macro, trend-following strategies can be a capital-efficient way to introduce a slightly negative-to-neutral correlated return stream, while preserving liquidity and minimizing cost. Historically, trend-following has produced strong diversification during most periods of market stress, delivering a negatively correlated return profile during the worst periods of equity drawdowns. Thanks to the underlying liquidity profile, trend-following strategies usually offer attractive daily and/or weekly liquidity terms.

Over the past 24 years or so, trend-followers (as proxied by the SG Trend Index) have produced an average correlation close to zero, which points to their strong diversifying benefits within the context of a total portfolio. Additionally, they offer exposure to commodities (and other idiosyncratic trends) which tend to be underweight in many investors’ portfolios. That said, trend following—most notably medium- and long- term trend-following—tends to suffer during periods of sharp market reversals and/or when markets whipsaw. On the other hand, these strategies do well during periods of sustained bullish and/or bearish trends.

Global macro strategies can exhibit high degrees of volatility over short periods of time, specifically more directional global macro strategies that take concentrated bets on, for instance, interest rates and commodity prices. More diversified global macro strategies, which include more hedges and relative value components —which we tend to prefer at NEPC—typically display more moderate volatility levels. We often see clients utilize global macro strategies along with other approaches to mute the overall volatility of their DS portfolio and provide a more balanced stream of returns, as global macro and trend-following tends to have a strongly uncorrelated profile compared to other parts of the portfolio.

At NEPC, we also believe that blending discretionary and systematic, including trend following, styles of investing within the global macro portion of the portfolio provides a more effective exposure to the global macro space, thanks to the two approaches’ complementary return profiles.

It is also worth noting that the return profiles of global macro and trend-following tend to have a positive skew (a larger right tail). This property also complements the negative skew return profile associated with equities in the rest of the portfolio.

b) Multi-strategy (Direct and Fund-of-Hedge Funds)

Multi-strategy direct hedge funds and fund-of-hedge-funds (FoHFs) can deliver an all-weather return profile due to the diversification of underlying strategies. The degree to which they are return-seeking or diversifying is driven by how much beta is tolerated in underlying funds in the case of FoHFs, or taken by underlying traders for multi-strategy direct hedge funds.

Clients who desire more liquidity, lower cost, and less headline risk tend to prefer FoHFs strategies over multi-strategy direct hedge funds. FoHFs also can give limited partners access to managers who are otherwise closed. Multi-strategy direct hedge funds offer higher returns than FoHFs as the latter have two layers of fees and are highly diversified.

When choosing a FoHFs manager, assessing the stability of the firm is important since FoHFs have not garnered the same level of assets that multi-strategy direct hedge funds have in recent years. FoHFs that have lost considerable assets under management may have experienced the departures of key personnel, or may be sourcing fewer new ideas than other FoHFs managers who have accumulated assets. However, too much fundraising by a FoHFs manager can lead to dilution of some of the closed capacity managers, and/or an increase in the number of managers utilized to the point where overdiversification can pose a concern.

Multi-portfolio manager platforms are a subset of multi-strategy hedge funds that utilize strict risk controls, a more siloed risk-taking structure, and pass-through fees. Strict risk controls are designed to force underlying portfolio managers to derive returns that are predominantly driven by idiosyncratic factors, while removing beta to broader market indexes and risk sensitivity to factors, including inflation, equity style, sector and/or industry.

The application of a systematic risk management process applied to fundamental strategies such as equity long/short has been a significant innovation in the hedge fund industry. It has made these strategies more diversifying to investors who take these risks elsewhere in their portfolios. This process ratchets up the proportion of the funds’ return driven by idiosyncratic factors more significantly than an active long-only equity fund could achieve, or even a long/short fund that allows factor risk to build up across positions. As a result, multi-portfolio manager platforms can be diversifying to the rest of an investor’s portfolio.

Multi-portfolio manager platforms have delivered strong absolute- and risk-adjusted returns, a low correlation to other asset classes, and have offered protection in volatile market environments. However, they come with unique risks/drawbacks, including deleveraging risk, high fees and poor liquidity. Due to the strict risk controls applied to underlying strategies, these approaches apply significant leverage to scale returns. In addition, these strategies are primarily focused on generating high returns because they need to cover the high fees they charge to produce competitive returns net-of-fees.

Multi-PM platforms are best suited for clients who are interested in return-seeking DS and are willing to bear the risks that come from high leverage utilization and headline risk. Multi-strategy direct hedge funds that are not run with all the attributes of multi-PM platforms can have higher beta and correlation to other asset classes but can offer more LP-friendly liquidity and fee terms.

Multi-strategy hedge funds can be difficult to evaluate given the large number of individual risk takers and various strategies that comprise them. At NEPC, we recommend comparing these strategies across a few key areas: talent acquisition, risk management capabilities, potential for forward-looking alpha generation, and fund-raising discipline.

c) Event-driven

Manager selection is important in allocating to event-driven strategies, as portfolios tend to have flexible mandates and may be very idiosyncratic, which can result in varying return experiences. Additionally, while exposure to multiple sub-strategies within event-driven can produce an all-weather return across economic environments, certain sub-strategies as standalone allocations can exhibit cyclicality and directionality versus other diversifying hedge funds. Therefore, at NEPC, we emphasize managers that can perform during both benign and turbulent markets, targeting a differentiated opportunity set and employing a nimble approach that can allow for opportunistic expressions of the portfolio when market conditions align.

While event-driven drivers of risk are unique and diversifying, exits and realizations can still be dictated by market events and pricing dynamics. Therefore, event-driven managers typically carry more credit and equity beta versus global macro and multi-strategy hedge funds. For example, general spread widening or heightened volatility may cause event-driven strategies to underperform other hedge fund strategies in these types of periods. However, event-driven tends to be highly opportunistic, leaning into market dislocation, which can set up strong outperformance in subsequent periods. Event-driven strategies are generally long biased, varying in liquidity, and can be an attractive option to increase the return potential within a diversifying allocation.

6. Constructing Portfolios with Diversifying Strategies

To bring this discussion to life, here is an example of how we have assembled diversifying allocations. We have calculated the returns using the median monthly return for each of the strategies on NEPC’s focused placement list.

All data is from 1/01/2006 – 9/30/2024

Annualized Return is net of NEPC’s estimated fees of 10 bps. There is no guarantee that the hypothetical performance will be achieved in the future or that an investment will not result in losses. Projected returns are hypothetical. Returns are calculated using the median monthly return from NEPC’s respective Focused Placement List for each strategy type (i.e. FOHF, Multi-strategy, etc.).

*The privates blended proxy is made of the following indices: 60% C|A Global All PE, 25% C|A Global Real Assets w RE, 15% C|A Global Credit.

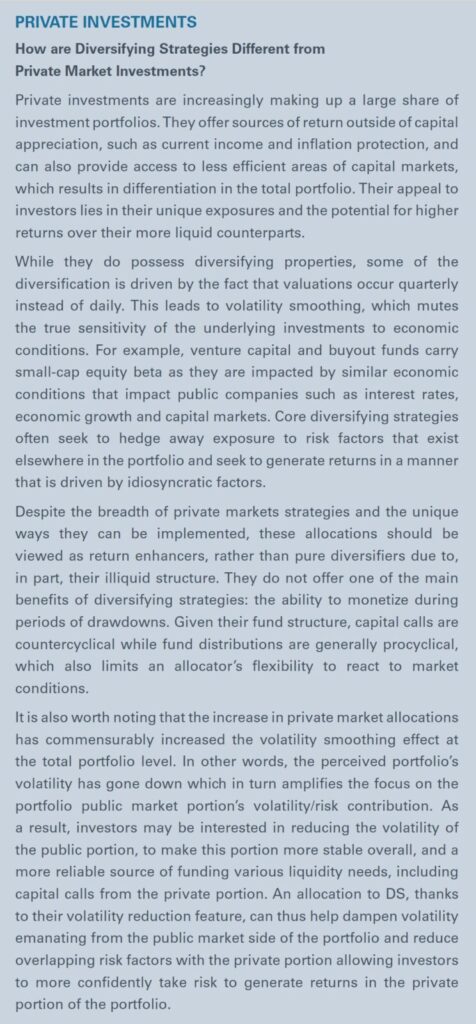

In exhibit 2 the orange box around “beta to 60/40” highlights the primary consideration in building various diversifying sample mixes. We include other measures of beta and correlation, and private investments funded from equities. The most diversifying mix, with the lowest beta to all benchmarks—mix 1—utilizes 100% global macro strategies, split evenly between systematic and discretionary global macro, which complement each other.

Mix 1 also has a negative downside market capture, illustrating the long-volatility profile of global macro strategies. We start to optimize for return, while keeping our beta constraint low in mixes 2 and 3. In addition, we are cognizant of other constraints that investors have when establishing strategy allocations. For example, while multi-strategy hedge funds have produced strong risk-adjusted returns and low beta/correlation, they often come with high fees, poor liquidity and deleveraging risk, which are all reasons to diversify the strategy composition within a diversifying allocation.

Introducing return-seeking building blocks such as event-driven and multi-strategy increases beta and correlation to the benchmarks in mixes 2 and 3. While increasing the allocation to these strategies does raise beta/correlation slightly, it also enhances absolute and risk-adjusted returns, lowers the DS mix’s volatility level because these strategies are lowly correlated to one another, and improves upside market capture.

We believe portfolio mixes 2 and 3 will meet the needs of the broadest range of clients since most are not solely focused on minimizing beta/correlation with the rest of their portfolio, but also are interested in return potential. While we primarily emphasize the diversification benefits of these three portfolios, it is worth noting that all mixes 2 and 3 have outperformed a 60/40 portfolio on an absolute and risk-adjusted basis over this time period.

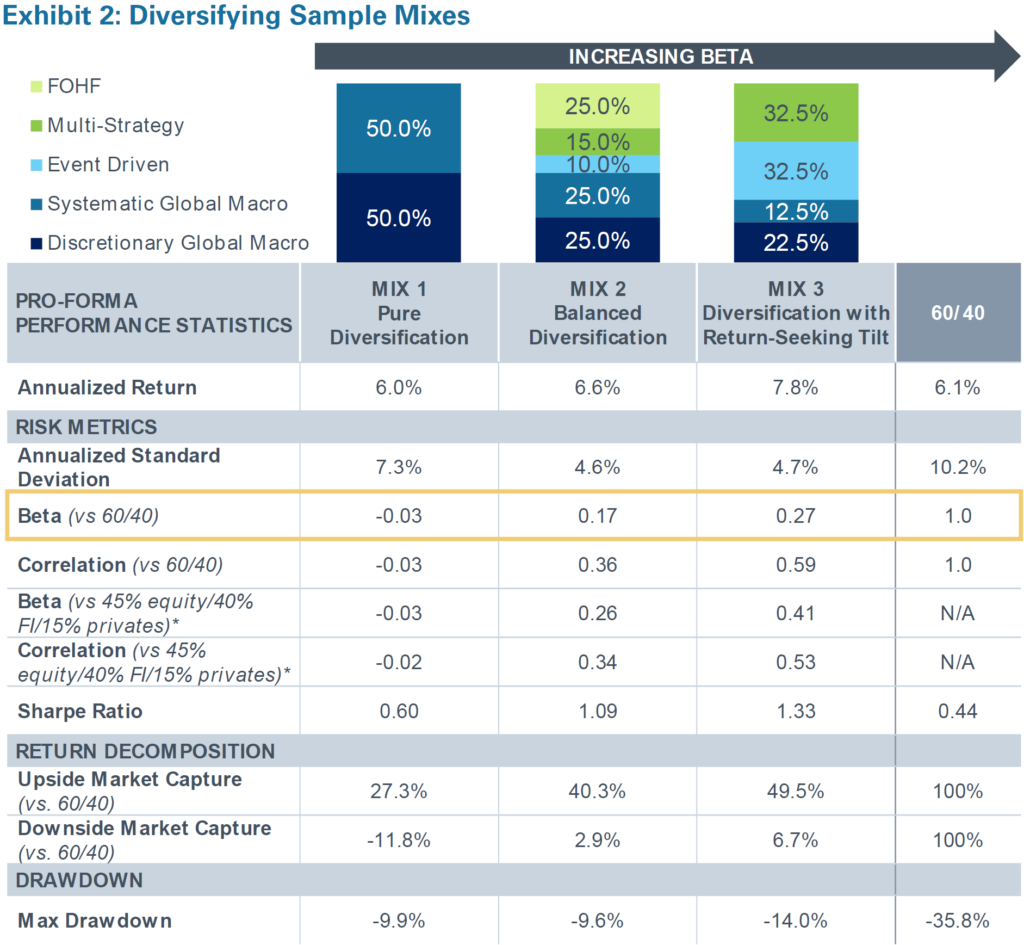

Since a major benefit of diversifying strategies is to protect in down markets, to serve as a funding source to buy other dislocated assets or to meet liabilities, as discussed earlier, in exhibit 3 we show how various hedge fund portfolio mixes have performed during market crisis environments.

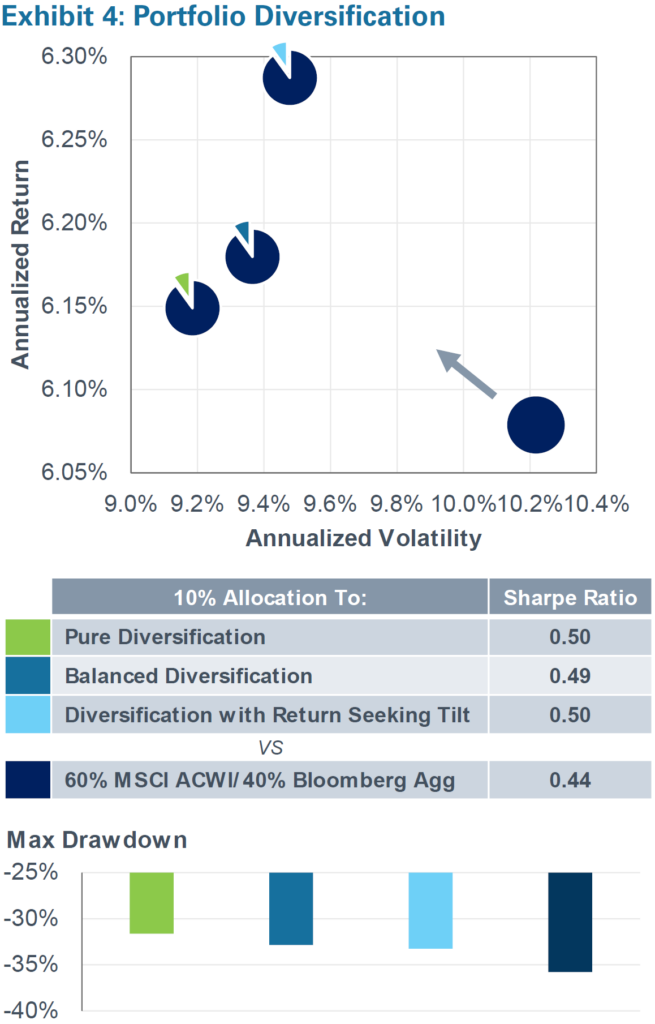

- Mix 1, which is the most diversifying and consists of 100% global macro, has performed the best in past market crisis environments, significantly outperforming a 60/40 portfolio.

- Mixes 2 and 3 have also significantly outperformed 60/40 portfolios in crisis environments. These portfolios also capture more upside in up markets as shown in the upside market capture in the table above and in the 2009 recovery scenario in exhibit 3.

- Event-driven strategies have some directional exposure to equity and credit markets, so increasing the allocation to these strategies in mixes 2 and 3 explains the higher downside capture and also the higher upside capture of these mixes.

Mix 2: Balanced Diversification (25% Discretionary Global Macro, 25% Systematic Global Macro, 25% FoHF, 15% Multi-Strategy, 10% Event-Driven)

Mix 3: Diversifying with Return Seeking tilt (32.5% Multi-Strategy, 32.5% Event-Driven, 22.5% Discretionary Global Macro, 12.5% Systematic Global Macro)

Due to the unique properties of the individual underlying strategies, we believe that a mixture of all the core strategies is the best approach to deliver an overall diversifying portfolio. This achieves the primary objectives of a diversifying allocation: a low correlation and beta versus a portfolio with stocks, bonds and private investments; diversification of risk factors; a funding source for liabilities and opportunities during market drawdowns; a positive expected return across a market cycle; and improved risk-adjusted returns for the overall portfolio.

Investors can tweak the inclusion/exclusion of underlying strategies or change the weights of the underlying strategies based on their specific objectives, unique portfolio requirements or constraints, and overall preferences, including sensitivity to taxes and fees, liquidity and headline risk.

To summarize the portfolio construction benefits that a diversifying allocation can have, exhibit 4 illustrates the impact of a 10% allocation to each sample mix on a 60/40 portfolio historically. Here, we can observe the impact of diversifying strategies on significantly limiting drawdowns and improving the total portfolio’s risk-adjusted performance.

The solid dark blue circle on the bottom right represents a 60/40 portfolio. The other three portfolios are comprised of 90% 60/40 and 10% allocations to each of the three diversifying sample mixes

7. For Stakeholders and Governing Bodies

After considering concentrated risks that exist elsewhere in their portfolio along with their overall objectives and risk tolerance, investors should set clear parameters around the diversifying allocation in terms of risk and return targets. Importantly, expectations for risk/return targets should be clearly understood and specified across a variety of market environments.

For example, investors should expect strong downside protection from their DS allocation during periods of market stress. We also suggest that investors set these expectations at the inception of their DS program in order to minimize emotional biases during periods of market drawdowns. This exercise, which includes obtaining an accurate picture of aggregated risks at the total portfolio level, will help investors finetune the weights of the underlying strategies within the DS allocation and judge the performance of the diversifying allocation more objectively moving forward.

The primary role of DS is to provide diversification within the context of a total portfolio. To that end, we emphasize focusing on correlation and beta targets to the rest of the portfolio. To increase the chance that the allocation will stabilize portfolio returns over a full market-cycle, and to reap the benefits around utilizing DS to fund opportunities and source liabilities in drawdown environments, it is also important to look specifically at performance across a range of macroeconomic environments, utilizing measures such as downside-market capture or scenario analysis.

Investors should also consider return targets for the overall diversifying allocation and for analyzing the performance of individual underlying managers. Possible benchmarks include cash plus, HFRI indexes, custom peer groups, blended benchmarks, and beta-adjusted benchmarks for more return-seeking strategies/portfolios. Investors should clearly set long-term correlation and return targets. If investors are not clear around the beta and (low) correlation this allocation should have to the rest of their portfolio, they may build an allocation that they think is diversifying but ends up drawing down in a correlated fashion with the rest of their portfolio. In some cases, investors benchmark DS to an ill-suited, return-seeking benchmark, like the S&P 500. This can lead to investors getting frustrated with the diversifying allocation and abandoning it before it can provide value to their overall portfolio.

Conclusion

Diversifying strategies are diversifying to stocks, bonds, and private investments because their exposures are different. More importantly, the most diversifying strategies utilize investment processes that produce returns driven by idiosyncratic risk rather than factor risk.

To achieve the diversifying characteristics—low correlation and beta versus stocks, bonds and private investments, diversification of risk factors, positive expected return across a market cycle—we believe a mix of core DS is most effective. The core options that we have outlined can be combined to effectively meet these goals. The combination of these diversifying strategies offers an all-weather approach to varying market conditions, with the flexibility to selectively and opportunistically manage exposure.

To learn more on these approaches or how to implement them within your portfolios, please contact your NEPC consultant.

Raj Palekar, Senior Investment Analyst, contributed to this piece.