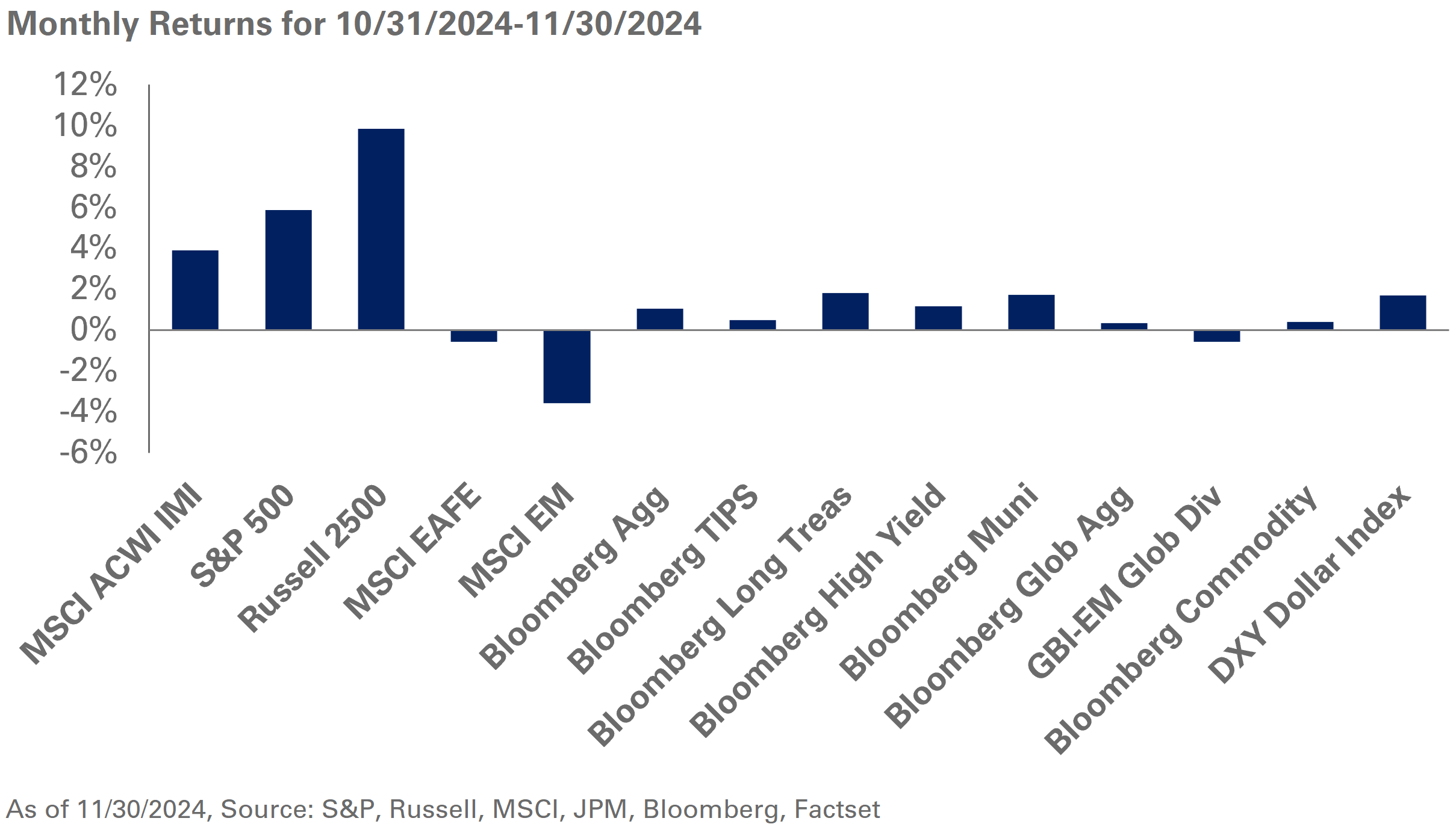

Following the U.S. elections, markets were quick to digest a mix of higher growth but potentially inflationary policies around tariffs, taxes, immigration and deregulation. In response, U.S. equities significantly outperformed in November with small-cap stocks leading the charge in anticipation of a more favorable regulatory and tax environment; the Russell 2000 Index was up 11% in November. During this period, large-cap equities also held their own with gains of 5.9% for the S&P 500 Index – its largest monthly return so far in 2024.

In contrast, markets outside the U.S. were challenged by a stronger U.S. dollar and the prospect of more protectionist foreign and trade policies from the U.S., particularly towards China; the MSCI EAFE and MSCI Emerging Markets indexes underperformed, falling 0.6% and 3.6%, respectively, in November.

As expected, the Federal Reserve cut interest rates by 25 basis points to a range of 4.50%-4.75%, citing continued progress in curbing inflation and normalization in labor market data. That said, fixed-income returns experienced only modest gains as markets weighed potential inflationary implications of policy proposals and priced in fewer rate cuts in 2025. In response, 10- and 30-year Treasury yields fell 11 and 12 basis points, respectively, causing long-duration indexes to outperform; the Bloomberg Long Treasury Index added 1.8% last month.

U.S. fixed-income markets also benefitted from the broad risk-on sentiment with option-adjusted spreads continuing to tighten across the credit spectrum. Notably, index-level spreads in the high-yield space fell below 270 basis points after declining 17 basis points in November, fueling a 2.6% return for the Bloomberg U.S. High Yield Corporate Index.

Within the real assets complex, the Bloomberg Commodity Index eked out a monthly gain of 0.4%, while underlying commodities exhibited significant return dispersion. In a change of pace, spot gold prices retreated 3.4% as U.S. dollar strength and greater clarity around geopolitical uncertainties weighed down the metal.

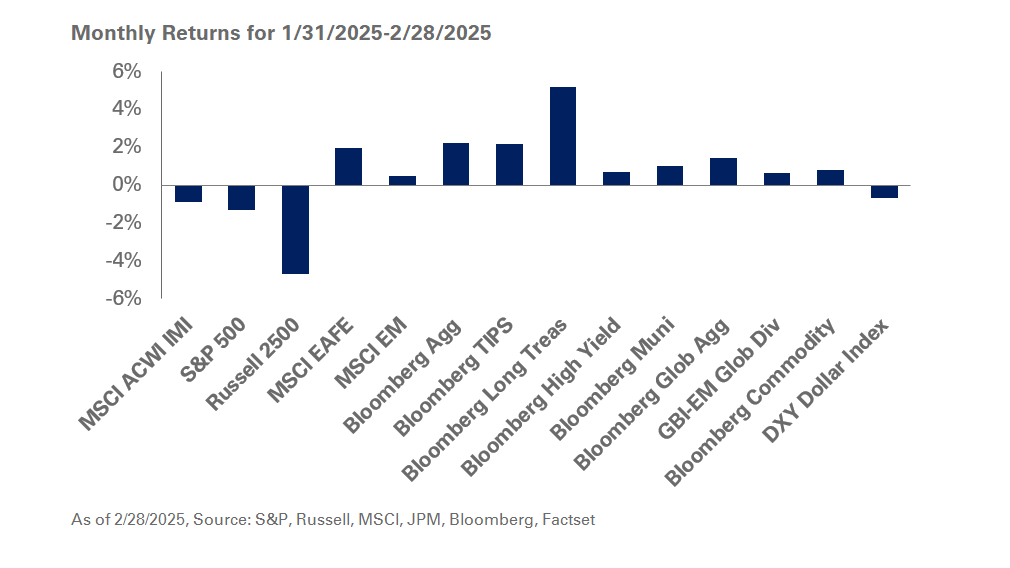

We encourage neutral-duration positioning relative to strategic targets given the current interest rate environment. In addition, we suggest investors consider high-yield bonds as a liquidity source within portfolios and look to reduce overweight positions. We remain steadfast in our recommendation to hold a blend of S&P 500 and value exposures within U.S. large-cap stocks. We encourage investors to remain disciplined and stick to long-term strategic asset allocation targets. At the same time, we urge our clients to keep liquidity on hand to rebalance should the market overreact to any surprise headlines in the coming months.