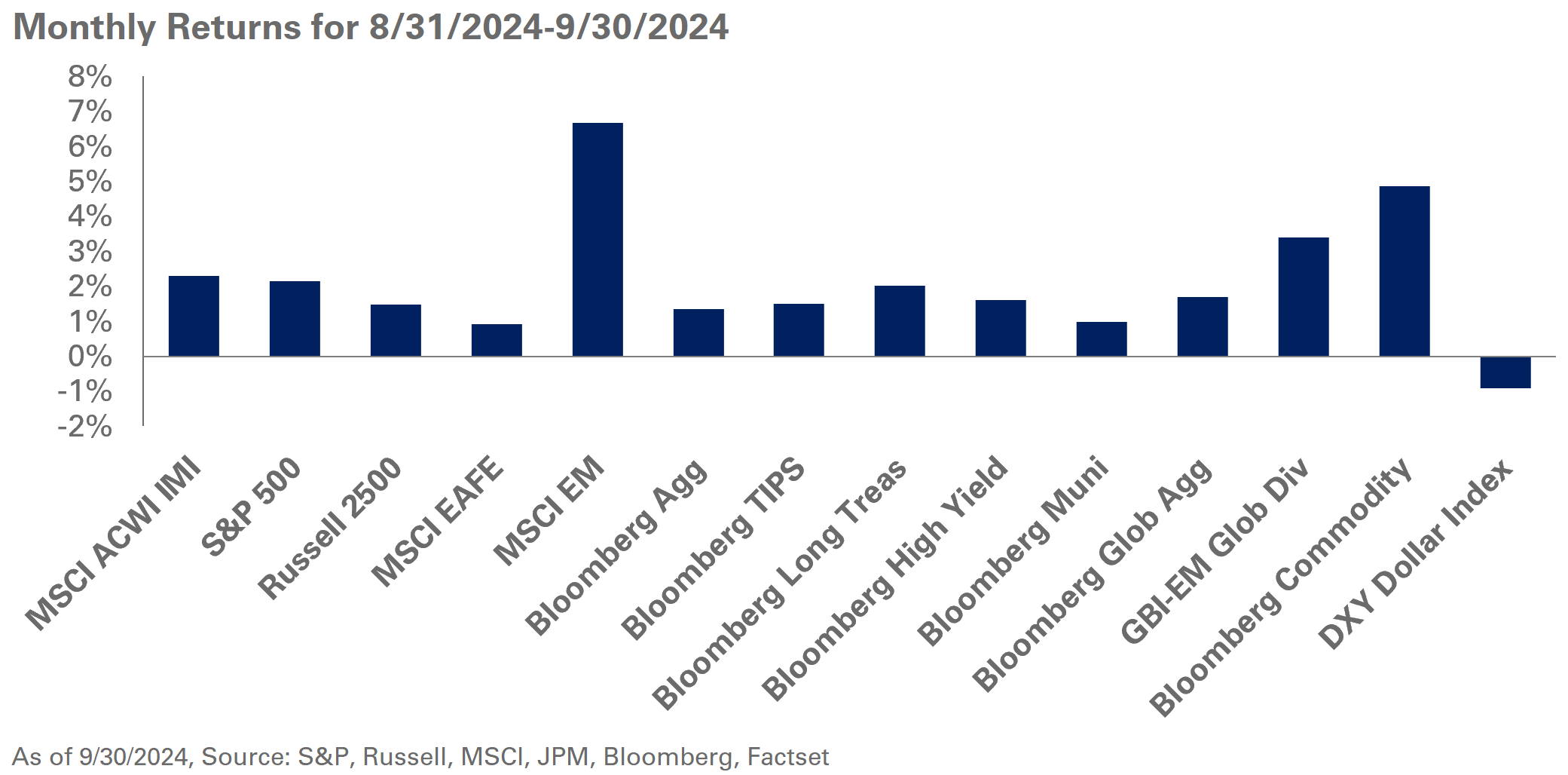

Stocks enjoyed another month of gains in September as positive economic momentum fueled the bull market. U.S. stocks finished September up 2.1% with growth outperforming value by 1.4%. Small-cap stocks eked out gains of 0.7% for the month, lagging their large-cap counterparts by over 10% year-to-date. Global stocks returned 2.3% with the EAFE Index up a modest 0.9%, while emerging markets gained 6.7% bolstered by a whipsaw rally in Chinese stocks amid news of long-awaited major economic stimulus.

Key economic data underscored a growing U.S. economy with real GDP growth at 3% for the second quarter, up from 1.6% in the prior quarter and higher than the 2.4% a year earlier. Inflation for August (reported in September) met expectations, with headline inflation rising 0.2% for the month, reflecting a 2.5% year-over-year increase.

Finally, employment held steady with weekly jobless claims and job vacancies showing no weakness; while recent monthly reports have shown an uptick in the unemployment rate, the data for September showed an addition of 254,000 jobs, soundly beating expectations by 112,000.

The Federal Open Market Committee met in September and, citing weakness in the jobs market, cut interest rates by 50 basis points to set the range of the federal funds rate to 4.75%-5%. As inflation seemingly wanes, the Federal Reserve is changing gears to focus on the labor market as part of its dual mandate to stabilize prices and strive towards full employment. The updated Fed dot plot survey of interest rate expectations of FOMC members shows two more cuts of 25 basis points each in 2024; it also indicates expectations for the long-run interest rate to rise to 2.9% from 2.5%.

The two-year U.S. Treasury yield—a proxy for short-term market expectations for Fed interest rate policy—declined to 3.6% from 3.9% in September. Long-bond yields were also lower in September with the 10-year yield at 3.8% and the 30-year at 4.1%. During the same period, credit markets continued to show strength with spread levels tightening further with investment-grade spreads at 89 basis points and high-yields spreads at 295 basis points. We suggest using high-yield bonds as a source of portfolio liquidity, given the current spread levels and expectations for lower base rates moving forward.

Meanwhile, oil was the only major outlier in September, ending the month in the red. WTI Crude Oil spot prices were down 8.6% to $68/barrel. Despite the downward pressure from oil, commodities finished the month up 4.9%.

With recent bouts of market volatility, we suggest investors remain disciplined and be prepared to rebalance positions should we see a more significant sell-off. We encourage maintaining a fundamental investment perspective and holding safe-haven fixed-income exposure in line with long-term strategic asset allocation targets. We continue to advocate investors hold a blend of S&P 500 and value exposure within U.S. large-cap stocks. In addition, we remain steadfast in our recommendation to introduce a dedicated U.S. TIPS allocation given current real interest rates and breakeven inflation levels.