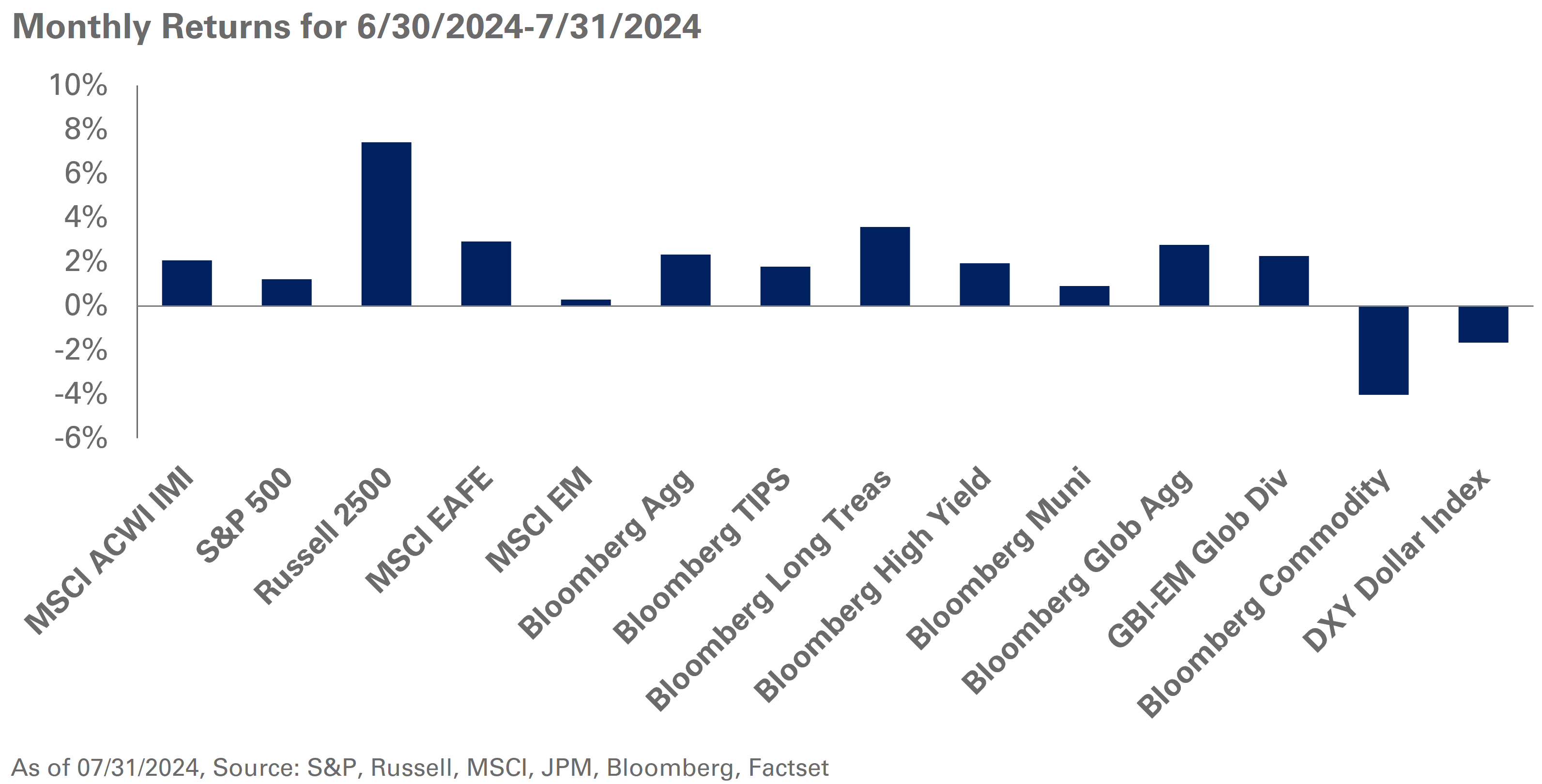

July witnessed the “great rotation” in U.S. equities. Small-cap stocks led the way, with gains of 10%, following months of lackluster performance. In addition, value-oriented equities surged with the Russell 1000 Value Index up 5.1%, while the Russell 1000 Growth Index was down 1.7%. During this time, the S&P 500 was able to eke out a gain of 1.2% as the prices of technology-oriented companies buckled under the strain of sky-high earnings expectations. Outside the U.S., the MSCI EAFE Index, supported by a stronger Yen and Euro, generated a 2.9% return for the month. The MSCI Emerging Markets Index gained a paltry 0.3% in July, with large index exposures linked to Nvidia moving lower.

Meanwhile, two- and 10-year Treasury yields fell 46 and 32 basis points, respectively, with the yield curve becoming less inverted over the course of the month. Government bond yields across the world moved lower, reacting to softer inflationary prints and mixed economic data. In addition, the Federal Reserve left rates unchanged in July, but left the door open for a potential rate cut in September. Long-duration fixed income was in the black as the 30-year Treasury yield fell 20 basis points in July. During this period, credit markets were relatively quiet, benefiting from lower interest rates while credit spreads were largely unchanged.

Elsewhere, real assets were a mixed bag in July with WTI crude oil prices down 10% amid concerns around global economic weakness; gold rose 3.6%, responding to geopolitical tensions and political uncertainty in the U.S. During this period, REITs were a bright spot, up over 7%, benefiting from hopes of lower interest rates.

As the presidential election season moves into a higher gear, we caution against kneejerk reactions to a fast-paced news cycle and the volatile political landscape. We encourage maintaining a fundamental investment perspective and holding safe-haven fixed income exposure in-line with long-term strategic asset allocation targets. We continue to recommend investors hold a blend of S&P 500 and value exposures within U.S. large-cap stocks. In addition, we solidly stand by our recommendation to introduce a dedicated U.S. TIPS allocation given current real interest rates and breakeven inflation levels.