Increases in U.S. Treasury rates contributed to an uptick in liability discount rates and improved funded ratios for many U.S. corporate pension plans in the third quarter of 2023. However, for the second straight quarter, losses from return-seeking assets contributed to declines in funded ratios, offsetting gains from the decline in liabilities. During the quarter, global equity markets struggled as inflation remained elevated and the Federal Reserve continued to hike rates. During the three months ended September 30, the Fed increased the Fed Funds Rate by 25 basis points. Estimated discount rates for pension liabilities, based on long-duration fixed-income yields, also rose, reaching their highest levels in more than five years. We estimate that the funded status of a total-return plan increased 5.9%, and the LDI-focused plan experienced a funded status decrease of 0.3% in the third quarter.

Rate Movement Commentary

Short- and long-term interest rates moved higher for the three months ended September 30th. The 30-year Treasury yield increased 88 basis points during the quarter to 4.73%. Offsetting the rise in yields was a 15 basis point decline in long credit spreads. Taken together, higher Treasury yields in the third quarter resulted in an increase in pension discount rates, with the rate for the open total-return plan increasing 66 basis points to 5.89% and the discount rate for the frozen LDI-focused plan rising 64 basis points to 5.83% as of September 30.

Plan Sponsor Considerations

Equity and fixed-income markets experienced negative performance in the third quarter of 2023 . Plan sponsors may find the current market environment difficult as stocks and bonds remain volatile though higher interest rates have generally been positive for plan funded status. Notably, long-term interest rates are materially higher year-to-date, while strong equity market returns earlier in the year provided an opportunity for total-return plans to (re)consider LDI to better meet objectives. For certain plan sponsors, higher-funded status levels are also providing a tailwind in the form of lower required contributions and declining PBGC variable-rate premiums. NEPC consultants are available to discuss the benefits and cost of various pension finance and derisking strategies.

Market Environment and Yield Curve Movement

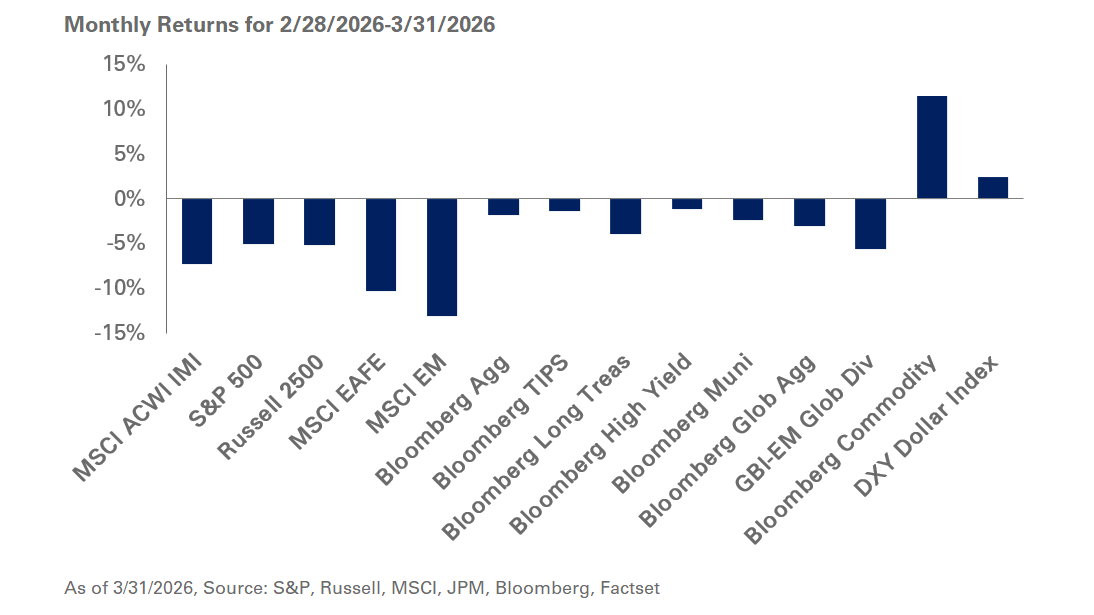

U.S. equities decreased 3.3% in the third quarter of 2023. Non-U.S. developed market stocks modestly underperformed the U.S. as the MSCI EAFE decreased 4.1% during the quarter; the MSCI Emerging Market Index decreased 2.9% during the same period.

Treasury yields increased and the yield curve remained inverted. The 30-year Treasury yield was 88 basis points higher for the quarter, resulting in a total return of -11.8% for the Barclays Long Treasury Index. During the same period, the Barclays Long Credit Index declined 7.2%.

Related Insights